Credit Cards

Whether you’re transferring a balance, looking to spread out the cost of purchases, or need extra flexibility, we’ve done the hard work for you.

Explore the UK Credit Cards market

Compare data from 140 Credit Cards

Learn which type of card is right for you

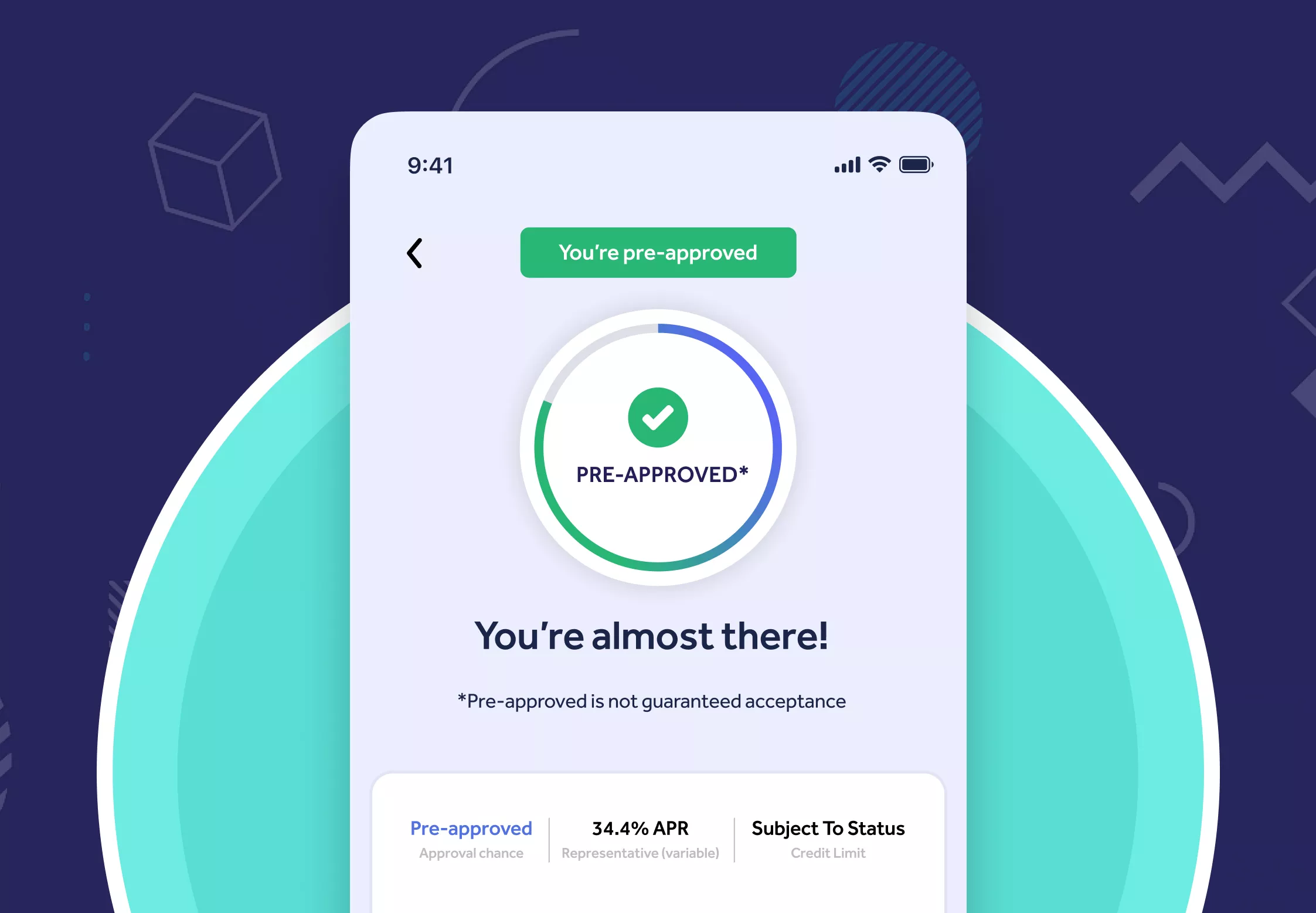

Check your eligibility without affecting your credit score

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Cash Back

Rewards

Balance Transfer

0% Purchases

Low Interest

Credit Building

For Travel

No Annual Fee

We compare credit cards from 40+ trusted UK providers.

We provide a research based view of credit cards available in the UK, using publicly available data from over 40 providers. This information was compiled in February 2026 and is not financial advice.

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender. Find out how this site works.

Best UK Credit Cards in February 2026.

We conduct independent, ongoing research into the UK credit card market, examining key features like balance transfer rates, cashback offers, travel perks, and other rewards. Our analysis includes popular and lesser-known cards that offer strong value based on publicly available data. We’ve highlighted standout options in each category based on our editorial criteria, but you can also explore and compare key features across a wide range of UK credit cards in our full comparison view.

Cashback

Representative APR

35.0% APR (variable)

Purchases

29.4% (variable) p.a.

Balance Transfers

29.4% (variable) p.a. (3% fee)

Account Fees

£25

Representative Example: At an assumed credit limit of £1,200 with a purchase rate of 29.4% (variable) p.a., and a fee of £25 p.a., most accepted customers get a rate of 35.0% APR (variable).

Representative APR

29.4% APR (variable)

Purchases

29.4% (variable) p.a.

Balance Transfers

29.4% (variable) p.a. (3% fee)

Account Fees

£0

Representative Example: At an assumed credit limit of £1,200, with a purchase rate of 29.4% (variable) p.a., most accepted customers get a rate of 29.4% APR (variable).

Representative APR

29.0% APR (variable)

Purchases

29.0% (variable) p.a.

Balance Transfers

Not Available

Account Fees

£0

Representative Example: At an assumed credit limit of £1,200, with a purchase rate of 29% (variable) p.a., most accepted customers get a rate of 29.0% APR (variable).

Representative APR

37.8% APR (variable)

Purchases

29.9% (variable) p.a.

Balance Transfers

29.9% (variable) p.a. (3% fee)

Account Fees

£4 per month

Representative Example: At an assumed credit limit of £1,200, with a purchase rate of 29.90% (variable) p.a., most accepted customers get a rate of 37.8% APR (variable).

Rewards

Representative APR

36.1% APR (variable)

Purchases

29.4% (variable) p.a.

Balance Transfers

29.4% (variable) p.a. (3% fee)

Account Fees

£0 for year 1. Then £30 p.a. from year 2 onwards.

Representative Example: At an assumed credit limit of £1,200, with a purchase rate of 29.4% (variable) p.a., and a fee of £0 in year 1 and £30 per annum from year 2 onwards, most accepted customers get a rate of 36.1% APR (variable).

Representative APR

29.4% APR (variable)

Purchases

29.4% (variable) p.a.

Balance Transfers

29.4% (variable) p.a. (3% fee)

Account Fees

£0

Representative Example: At an assumed credit limit of £1,200, with a purchase rate of 29.4% (variable) p.a., most accepted customers get a rate of 29.4% APR (variable).

Representative APR

29.9% APR (variable)

Purchases

29.90% (variable) p.a.

Balance Transfers

29.90% (variable) p.a.

Account Fees

£0

Representative Example: At an assumed credit limit of £1,200, with a purchase rate of 29.90% (variable) p.a., most accepted customers get a rate of 29.9% APR (variable).

Representative APR

23.9% APR (variable)

Purchases

0% for up to 6 months, then 23.90% (variable) p.a.

Balance Transfers

0% for 6 months, then 23.90% (variable) p.a. (2.99% fee)

Account Fees

£0

Representative Example: At an assumed credit limit of £1,200, with a purchase rate of 23.90% (variable) p.a., most accepted customers get a rate of 23.9% APR (variable).

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Best Credit Card Providers

Amex UK

10 CARDS

Barclaycard

9 CARDS

Santander

5 CARDS

Tesco Bank

4 CARDS

HSBC (UK)

7 CARDS

Bank of Scotland

3 CARDS

UK Credit Cards Guide

What are credit cards? How do they work? How do you decide among cash back, travel points and other rewards options as well as maximising the value you get from your card? In this guide, we explain the different types of credit cards available in the UK and what to look out for when making a choice.

Before deciding to get a credit card and comparing the range of products on the market, it’s important to understand how credit cards work, the types of cards available, and what interest fees and other charges may apply. Additionally, given that UK credit card providers will run a hard credit check as part of their application process, it’s a good idea to understand how credit scoring works and make use of our eligibility checker. In this guide, you will:

Learn which type of card is right for you

Learn about credit scoring

Learn what an eligibility check is.

See FAQs

I know what I'm looking for

If you know what type of credit card you need, our research database contains over 130 cards with rates, fees and offers from UK financial firms which you can easily explore and compare. Alternatively, you can read our ‘Best UK credit cards’ where we break down the most popular.

What type of card is best for me?

About credit cards

Credit cards can be used for a variety of reasons and, when used responsibly, make a useful financial tool. When spending with a credit card, there is the option to delay payment and spread the cost of a purchase over a longer period. This flexible way of spending comes with many advantages, but is contingent upon using the card responsibly and making payments on time.

There are many different types of credit card that are designed by their issuers for different purposes and spending habits. For example, many providers will offer deals for transfering a balance from an existing card, to get cashback on purchases and other rewards, or simply to spend with. The interest charged will depend on the card, your credit score, and whether the balance is paid in full before interest fees apply.

Before deciding to get a credit card and comparing the range of products on the market, it’s important to understand how credit cards work, the types of cards available, and what interest fees and other charges may apply. Additonally, given that credit card providers will run a hard credit check as part of their application process, it’s a good idea to understand how credit scoring works.

What is a credit card?

Simply put, a credit card is a method of payment. However, rather than debiting funds from your current account each time you spend, the credit card company pays and sends you a bill for the balance each month. If you pay this off in full, you’ll pay no interest. You have to make at least the minimum payments required and, if you opt to pay a smaller amount, the remaining balance is carried over to the next month and you’ll be charged an amount of interest on that balance, until you repay it in full (unless you’re on a special 0% deal, which we’ll explain more about below).

At Mintify, we think a more useful or accurate term for credit card would be a ‘borrowing card’ or a ‘debt card’. Any spending on the card is actually running up a debt that you need to pay back rather than using credit that has been given to you.

Credit card FAQs

What is an APR (Annual Percentage Rate)?

Whenever you borrow money, you will typically find there’s an interest rate known as the annual percentage rate (APR). This rate is expressed on a yearly or ‘per annum’ basis and includes the total cost of borrowing, including interest charges and any annual fees that may apply.

A lower APR generally means cheaper borrowing costs. By understanding APR, you can make more informed decisions about which credit card suits your financial needs. Remember, if you pay off your balance in full each month, you will not be charged interest.

What is a Representative Example?

Representative APR is the rate that’s often shown in advertising for credit cards. It’s a standard compound rate, which means, it takes into account interest you’ll pay on top of interest, and any annual fees that apply.

To advertise a representative rate, at least 51% of applicants must be offered the stated rate, while the remaining 49% may receive a different rate (usually higher) or be denied. All lenders are required to display examples in the same way, which should make it easier to compare products from the various card issuers and assess the impact of annual fees to the overall cost of borrowing.

The Representative APR includes:

- The purchase (not transfer) rate and whether it’s fixed or variable.

- The representative APR and whether it’s fixed or variable.

- The amount of any annual fee (if applicable).

- An example borrowing amount of £1,200

It doesn’t include:

- Any other fees, such as default or transfer fees.

- The amount of credit you might be offered.

The cost of borrowing assumes spending the entire £1,200 on day one, repaying it in equal instalments over a year, and not borrowing more on the card. But this doesn’t imply a £1,200 credit limit.

Keep in mind that any rates, promotional offers, and the credit limit you may be offered are subject to security and credit checks when submitting a full credit application.

Which type of credit card is right for me?

By understanding your financial needs and knowing what to look for, you can find a credit card that suits your lifestyle and financial goals.

Before you start comparing credit cards, we recommend you consider a few key questions:

- How do I plan to use my credit card?

- Do I want to earn rewards or cashback on my spending?

- Do I want the credit card to be my primary payment method?

- Will I carry a balance month to month?

- Am I aiming to build or improve my credit score?

Having clear answers to these questions will help you identify the type of credit card that best suits your needs. For example, if your credit score is low, you might want to consider a Credit Building card. If you frequently travel, a Travel Rewards card could be beneficial. What we encourage you to avoid though, is carrying a balance month to month. Paying your balance off each month is going to maximise the benefit of having a credit card.

Am I eligible for a credit card?

Each credit card provider will have its own set of requirements for eligibility, but generally, you must be a resident of the UK and at least 18 years old to apply for a credit card. Some providers may impose a minimum age requirement of 21 or older. Additionally, different providers may have varying criteria such as minimum income levels.

It’s important to remember that applying for a credit card will leave a footprint on your credit file, potentially affecting your ability to secure future credit. We strongly recommend utilising a ‘soft search’ or eligibility check to determine which credit cards you qualify for and to assess your chances of approval before proceeding with an application.

How do lenders decide whether to give you a credit card?

In the majority of cases, passing a credit check is required in order to obtain a credit card. It allows lenders to assess the level of risk involved in lending to you, taking into consideration your income and financial obligations (affordability). Each lender has it’s own set of criteria, meaning acceptance by one does not guarantee acceptance by another.

To increase your chances of approval, it is advisable to use an eligibility checker before applying. All credit card providers will run a hard credit check as part of their application process, regardless of the outcome, which leaves a footprint on your credit report, potentially impacting your ability to obtain credit in the future, especially if multiple applications are made within a short timeframe.

If you check your eligibility for a card, this will only involve a soft check and won’t affect your credit score.

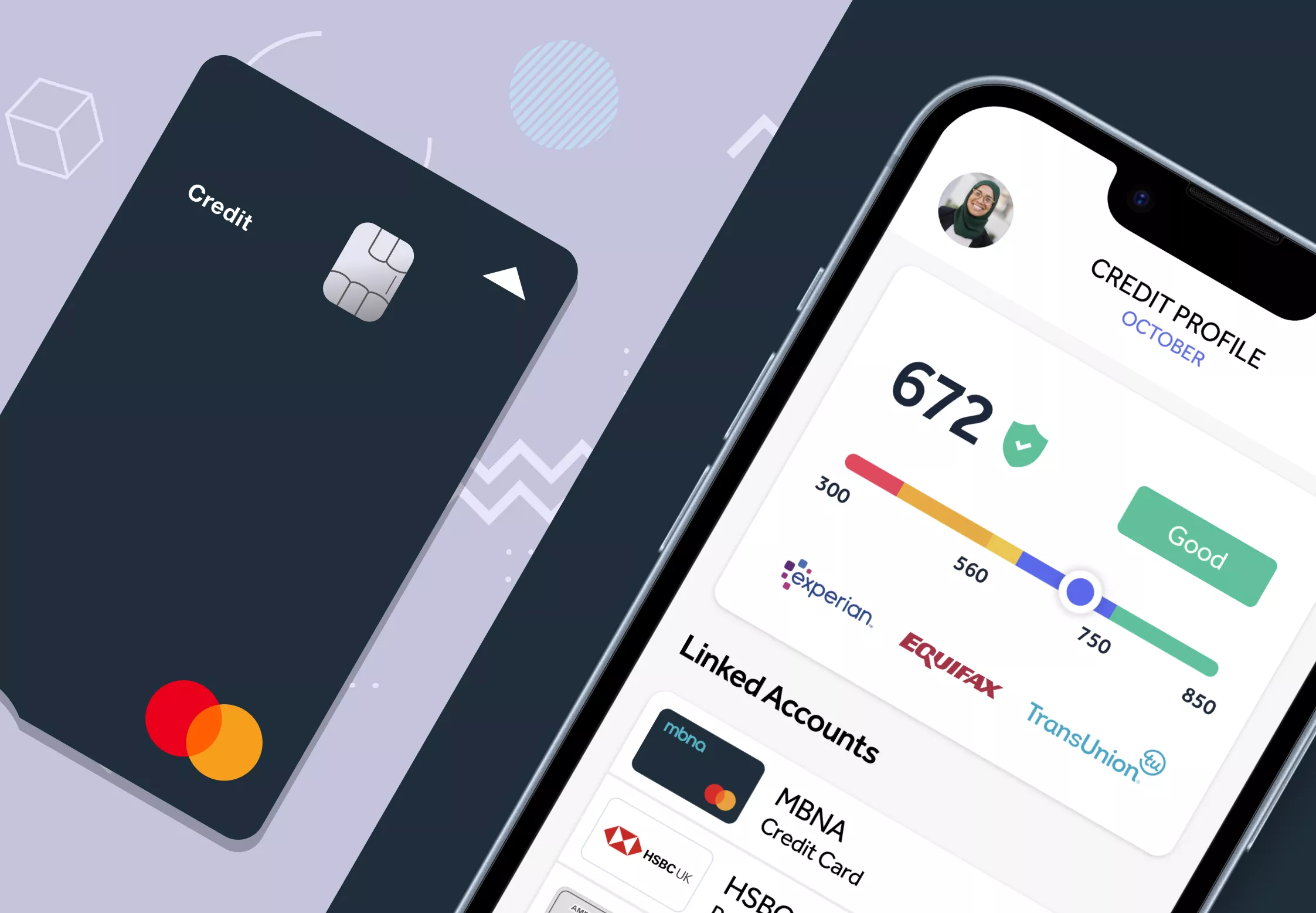

For more information on how credit scoring works, you can

What is a credit score?

Credit scoring is a process used by credit card companies and other lenders to make a decision as to whether or not they want to lend to you. This process is largely based on information they get from the credit reference agencies ( Equifax, Experian and TransUnion) who hold information about your credit history. They will also use information from your application form, and data from any accounts you’ve had with that financial firm in the past.

In general, having a positive record of repaying debt on time significantly increases your chances of approval compared to a history of missed payments.

Read more about how credit scoring works and how to check your credit report for free.

How does a credit card impact my credit score and can I get a card with a bad score?

Your credit score will determine your eligibility for a credit card and ability to benefit from cards with better interest charges than others. Simply put, a higher credit score indicates lower risk, making lenders more likely to approve your credit application and offer you better terms.

When you apply for a credit card, there will be a hard check against your credit file so, before you get started, be sure that you have selected the right card for you. We also strongly recommend utilising a ‘soft search’ or eligibility check to determine which credit cards you qualify for and to assess your chances of approval before proceeding with an application.

If you use your card responsibly, a credit card can actually improve your credit score. Responsible use demonstrates that you can handle credit well, you’re responsible with payments and if, you don’t continuously max out your credit card, you can improve your credit utilisation ratio. On the other hand, missing payments and carrying a balance consistently from month to month can hurt your credit score, potentially affecting your ability to secure future credit.

Getting a card with a bad credit score is still possible. Check our Credit Builder cards to specifically help you with this so that you can rebuild your credit rating responsibly.

What if my application for a credit card is rejected?

Getting rejected for a credit card can be confusing since lenders aren’t obligated to explain why. It could be because of a poor credit history or if they consider you a risky borrower. Rejections can negatively impact your credit score, especially if you apply for multiple cards in a short period.

To help avoid this, we recommend using a credit card eligibility checker. It allows you to assess your chances of being accepted for various credit cards without affecting your credit score. A good eligibility checker will provide a service that works with a panel of providers to understand their specific criteria and match your circumstances. This ensures quotability is as accurate as possible before submitting an application.

Do I have to pay interest and fees?

If you choose a credit card without an annual fee—and there are many available—and consistently pay off the balance in full before the interest-free period ends (typically 56 days), you’ll avoid paying any interest or incurring late payment fees.

If you plan to carry a balance from month to month, you’ll incur interest charges, and missed payments will result in additional fees. It’s crucial to fully understand the terms, conditions, interest rates, and fees associated with your card. By staying informed and spending responsibly, you can avoid unnecessary costs and ensure your credit card serves you, rather than the other way around.

Can credit card interest rates change?

Most credit cards come with a ‘variable APR’, which means that the interest that lenders charge on borrowing (the outstanding balance on a credit card) can fluctuate depending on market conditions. Your lender is obligated to inform you if they plan to change your credit card APR.

Alternatively, you can opt for ‘fixed APR’ cards where lenders guarantee that the rate will remain unchanged for a certain period, although these cards are less common and generally come with higher interest rates.

How can I manage my credit card responsibly?

When used responsibly, credit cards can be a highly beneficial financial tool. However, if misused, they can lead to significant harm with long-lasting effects. Therefore, it is generally advisable to:

- Understand interest rates and charges

- Pay off the full balance

- Manage credit utilization

- Build and maintaining a good credit score

- Use credit wisely

- Be aware of security and fraud prevention

- Maximise rewards and benefits

- Use balance transfers and consolidation wisely

- Manage multiple cards with care.

Take the time to read our full guide on how to use your credit card responsibly to avoid debt, and build a positive credit history in the UK.

What is a balance transfer and how does it work?

Balance transfer credit cards can be a useful tool to use if you’re looking to manage your debt more effectively. These cards allow you to move your existing balance from one or more credit cards to a new card, often with an introductory 0% interest period. This can help you save significantly on interest payments, making it easier to pay off your debt faster. However, this is only worthwhile if you are able to actually pay off the balance during the introductory period so that you can benefit from interest free rates.

Avoid common mistakes when selecting your balance transfer credit card such as not understanding how long the 0% interest free period lasts and not being able to clear your balance during that period – which is the main purpose and benefit of this card.

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity

Editor, Credit Cards: Michelle Blackmore

Last Updated: February 15, 2026