How to choose a credit card in the UK

Editor, Consumer Finance: Michelle Blackmore

Last Updated: February 15, 2026

In This Article

Choosing a credit card is not just about finding a low rate or a tempting reward. It is about understanding how you plan to use it and matching that to the right type of card. The right choice can make spending more flexible, improve your credit score over time, or help you save money. The wrong choice can increase your costs or make debt harder to manage.

This guide explains how to decide which type of card may suit you, what to look for before applying, and how to use your credit card responsibly once it is open.

Step 1: Think about how you plan to use your card

Start by considering your main reason for wanting a credit card. Your answer will shape which products are most suitable.

- If you usually repay in full each month:

You may benefit from a rewards or cashback credit card. These cards can give you value back on everyday spending if you clear the full balance on time, avoiding interest.- If you expect to carry a balance for a few months:

A low interest or 0% purchase card could be more useful. These cards let you spread the cost of a purchase interest-free for a set period, as long as you keep up repayments.- If you want to pay off existing balances:

A balance transfer card lets you move debt from one or more cards to a new one with a 0% or lower rate for a fixed time. This can reduce interest costs while you focus on repayment.- If you want to build or rebuild your credit history:

Credit builder cards are designed for people with limited or poor credit history. They usually have lower limits and higher rates, but consistent use can improve your credit profile over time.

Knowing your main goal helps narrow the options before you compare fees, rates, and features.

Step 2: Understand the main credit card types

The UK market offers a wide range of cards, each designed for different situations.

- Balance transfer credit cards:

Useful if you already have credit card debt. You can move your balance to a new card with a 0% interest offer for a set period, often between 18 and 29 months. You will usually pay a one-off transfer fee, typically 2 to 5 percent of the amount moved. Paying off the full balance before the offer ends helps you avoid higher revert rates.- 0% purchase cards:

Designed for spreading the cost of new spending without interest for an introductory period. 0% purchase card are ideal for large expenses like a small home improvement project or travel bookings. Divide the total amount by the number of interest-free months to create a repayment plan that clears the balance in time.- Rewards and cashback credit cards:

Best suited for people who repay in full every month. Rewards can include cashback, loyalty points, or air miles. Some cards charge annual fees, so check that the benefits outweigh the cost.- Credit builder credit cards:

Credit builder cards are intended for people with little or no credit history, or those rebuilding after missed payments. Limits are usually lower and interest higher, but timely repayments can help demonstrate reliability to lenders.

Are you carrying an existing credit card balance?

If you’re carrying balances on other credit cards, a balance transfer credit card can help you pay it down faster by moving your balance to a new card with 0% interest for a set period. Using a balance transfer calculator helps you understand how much interest you could potentially save by transferring debt from your existing cards to a balance transfer card.

Step 3: Compare costs, rates, and features

Once you know the type of card that fits your needs, compare the total cost of using it. The representative APR shows how much interest you would pay over a year if you carry a balance. If you repay in full each month, the APR is less important since you avoid interest entirely.

Check the following before applying:

- APR and interest rate: The interest charged after any 0% period ends.

- Fees: Annual, balance transfer, cash advance, or foreign transaction fees.

- Introductory offers: These can be valuable, but they end. Always check the revert rate.

- Eligibility criteria: Credit score and income requirements differ by lender.

- Repayment flexibility: Minimum payment rules, direct debit options, and early repayment policies.

Even small differences in fees or rates can make a meaningful impact over time, especially if you plan to keep the card for several years.

Step 4: Check your eligibility before you apply

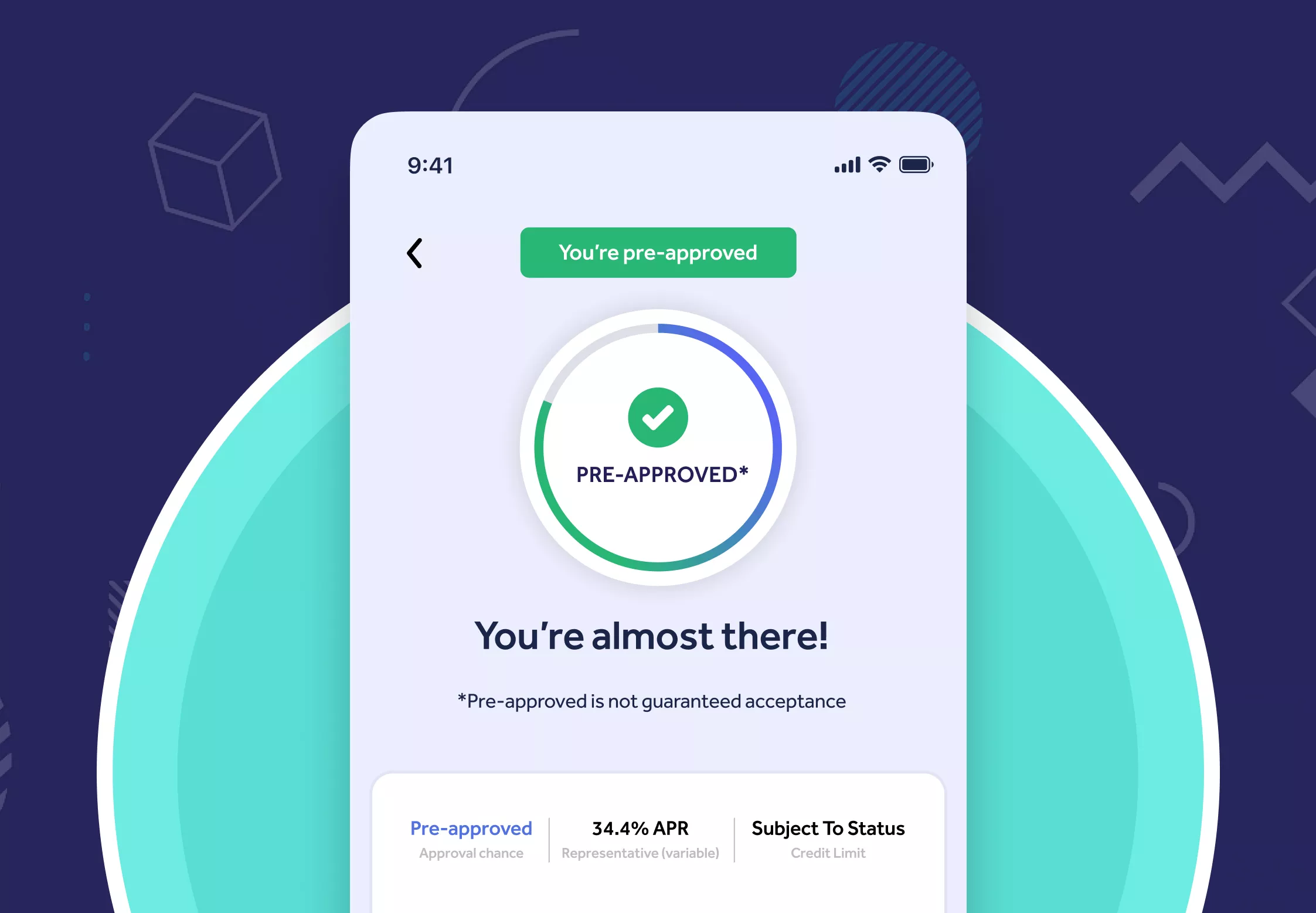

Each time you apply for credit, the lender runs a credit check. Too many hard checks in a short period can reduce your credit score temporarily. A credit card eligibility checker lets you see your chances of approval before applying. This uses a soft check, which does not affect your credit file.

Checking eligibility can help you find cards that suit your financial situation without unnecessary applications. It also allows you to focus on cards you are more likely to be accepted for, reducing the risk of rejection.

In general:

- People with higher credit scores may qualify for low interest or premium rewards cards.

- Those with average or limited credit may find mid-tier or starter cards more accessible.

- Applicants who are getting their first credit card may need a credit builder card at first, improving eligibility over time with responsible use.

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Step 5: Plan how you will repay

Having a credit card is useful only if it is managed well. Before applying, think about how you will keep repayments on track.

- Set up automatic payments to cover at least the minimum each month, avoiding late fees and protecting your credit score.

- Pay more than the minimum whenever possible to reduce your balance faster and save on interest.

- Budget for repayment if using a 0% purchase card or balance transfer card. Divide the balance by the number of interest-free months and pay that amount consistently.

- Check your statements regularly to spot errors or unfamiliar charges early.

Using a credit card responsibly can help improve your credit score over time, may make it easier to be approved for other credit products in future, and helps reduce the risk of long-term debt.

Step 6: Avoid common mistakes

Even experienced borrowers can make avoidable errors. Keep these points in mind:

- Do not apply for several cards at once. Each hard search can lower your credit score.

- Avoid withdrawing cash on a credit card. Cash advances often carry higher interest and no grace period.

- Always pay at least the minimum payment before the due date. Missed payments stay on your credit report for six years.

- Do not rely on a promotional period without planning for what happens after it ends.

- Watch out for “representative APR” differences. Only 51 percent of applicants must receive that rate, and others may be offered higher APRs.

Mintip: Strong financial habits matter more than the specific card you choose. Consistently paying your balance in full and on time, keeping balances low, and checking statements regularly will make any credit card work better for you.

Step 7: Match your credit card to your financial goals

Choosing the right credit card is easier when you focus on what you want it to do for you. Some examples:

- Building credit: A simple, low-limit card with on-time payments can build a record of reliability.

- Saving on debt: A balance transfer offer can reduce interest while you pay down existing balances.

- Financing a purchase: A 0% purchase period can spread the cost, but only if you repay before it ends.

- Earning rewards: Cashback or loyalty cards can return value if you always clear your balance.

Being clear about your goal helps you avoid overspending or using the wrong product for your situation.

Step 8: What to do if you struggle with repayments

If you find it hard to keep up with repayments, act early. Contact your card provider to discuss options such as repayment plans or interest freezes. You can also get free, confidential support from organisations like StepChange or MoneyHelper. Ignoring the problem can make it worse and damage your credit score further.

Frequently asked questions

How do credit cards work?

Credit cards let you borrow up to an agreed limit and repay later, either in full or in instalments. You receive a statement each month showing what you owe. Paying in full avoids interest, while paying part of the balance incurs interest at the stated rate. Responsible use can improve your credit score, while missed payments can harm it.

How do I get a credit card for the first time?

Start by checking your credit report to understand your current score. Use a free eligibility checker to see which cards you are likely to qualify for. If you have little or no credit history, look at credit builder cards designed for first-time applicants. Complete the application online and provide accurate personal and financial details. Once approved, use the card responsibly and make payments on time to build your credit profile.

How does a 0% purchase credit card work?

A 0% purchase card allows you to make new purchases without paying interest for a fixed introductory period. You still need to make at least the minimum payment each month. To avoid interest, clear the balance before the 0% term expires, after which the standard rate applies.

How do balance transfer credit cards work?

A balance transfer card lets you move existing credit card debt to a new card that offers a lower or 0% interest rate for a set period. You usually pay a transfer fee, which is a percentage of the amount moved. You then repay the balance during the promotional period to reduce interest costs. When the offer ends, the rate reverts to the card’s standard APR.

What is a soft credit check?

A soft credit check reviews limited information from your credit file to show your likelihood of being accepted for a product. It does not affect your credit score and is visible only to you. Lenders use soft checks for eligibility tools before a full application.

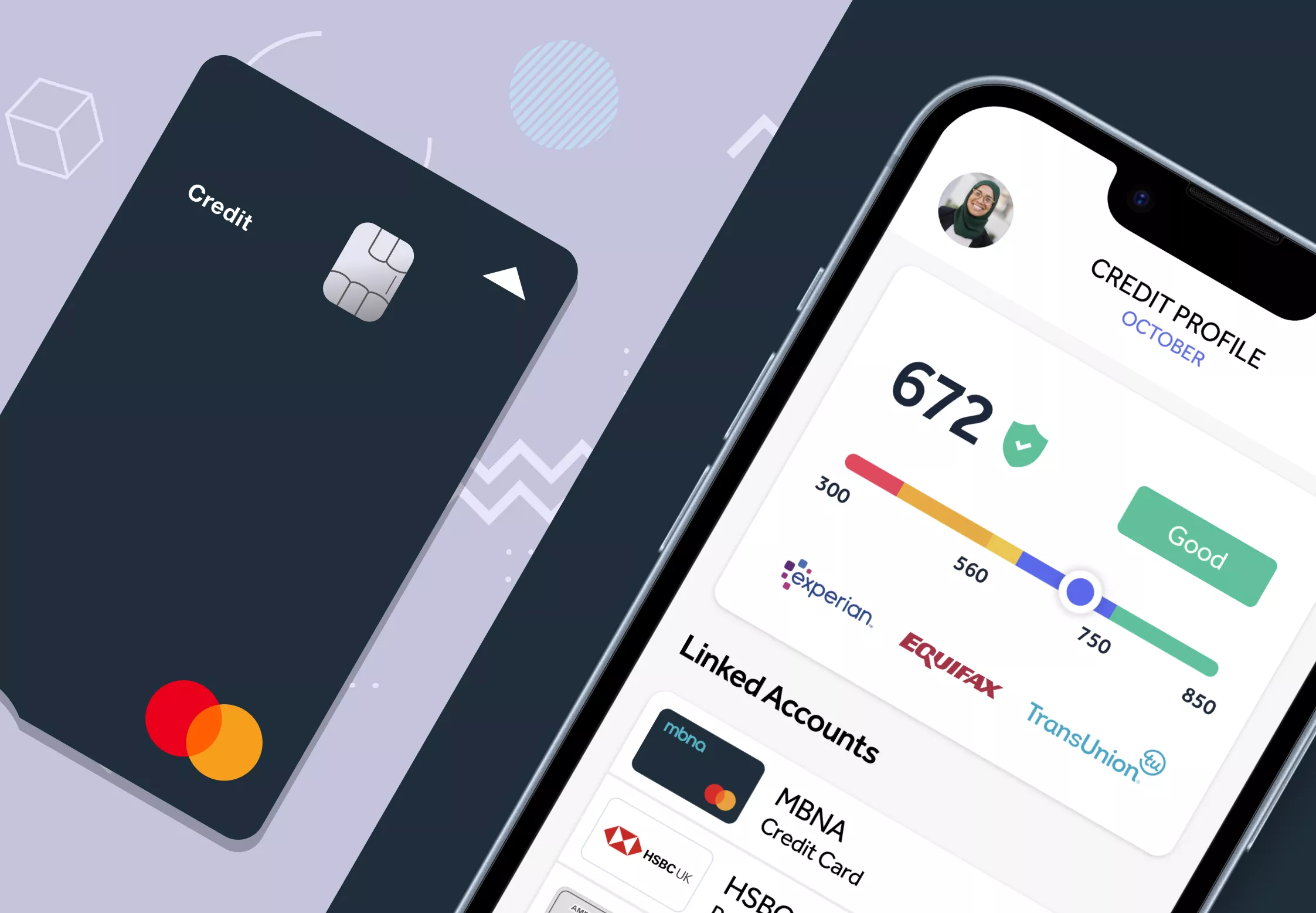

What is a good credit score?

Each credit reference agency uses its own scale. Generally, a score in the upper range of Experian, Equifax, or TransUnion ratings is considered good. A good score improves your chances of being approved for cards with lower rates and better rewards, but lenders also assess income, existing debts, and overall financial stability.

Key takeaways

- Understand why you need a credit card before choosing one.

- Match your repayment habits to the right type of card.

- Compare APRs, fees, and features carefully.

- Use eligibility checkers to avoid unnecessary hard searches.

- Plan repayments before spending to avoid high interest later.

- Seek help early if repayments become difficult.

Learning how to choose a credit card is about balance, not speed. The right card can simplify your finances, support good credit habits, and offer useful rewards. Take time to compare credit cards, read the terms carefully, and make sure the card fits your goals and budget.

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

What is a balance transfer fee?

How to do a balance transfer on a credit card