How much can you balance transfer?

Editor, Consumer Finance: Michelle Blackmore

Last Updated: February 6, 2026

In This Article

Quick Answer: A balance transfer limit is the maximum amount you can move to a new balance transfer card. It’s usually a percentage of the credit limit you are offered; typically around 90% to 95% but this varies by lender. Some lenders also set minimum transfer amounts or restrict transfers within the same banking group.

What is a balance transfer limit?

A balance transfer limit is the maximum amount you can move to a new balance transfer credit card. It is set by the new card provider and is usually linked to the credit limit you are offered on that card. The limit can be lower than your total credit limit, so you may not always be able to transfer everything you owe.

The balance transfer limit applies across all balances you move to that card. If you transfer more than one balance, the combined total cannot be higher than the limit set by the lender.

The balance you transfer may also include a balance transfer fee if the card charges one, which can increase the starting amount on your new card.

How lenders set your balance transfer limit

Lenders set your balance transfer limit based on a mix of product rules and your individual circumstances. The limit is usually a percentage of the credit limit you are offered on the new card, which can vary between credit card providers. Some cards allow you to transfer most of your available limit, while others set a lower cap.

Your income, existing credit commitments and overall financial profile are also considered. These factors help the lender decide how much credit to make available and how much of that credit can be used for balance transfers. You will only see the exact limit once you have been approved for the card.

Can you transfer your full existing balance?

You may be able to transfer your full balance, but this depends on the balance transfer limit you are offered. If your new limit covers the full amount, the entire balance can be moved. If it is lower, only part of the balance will be accepted and the remainder will stay on your existing card. Some lenders also apply product-specific caps, meaning you can only transfer up to a set percentage of your new credit limit even if you have available credit. You will see your confirmed balance transfer limit once your application is approved.

Minimum and maximum transfer amounts

Most balance transfer cards set minimum and maximum amounts that can be transferred. Minimums vary between lenders but are often around £100 per transfer. If the balance you want to move is below the product minimum, the transfer may not be accepted.

Maximum transfer amounts depend on the product rules and your approved balance transfer limit. Some cards cap the total you can transfer, while others may apply limits per transfer or per statement period. These conditions are set by the lender and will be shown in the product terms before you complete a transfer.

Example: how much you could transfer

Lets say you are approved for a new balance transfer card with a £3,000 credit limit. If the card allows balance transfers up to 95 percent of your credit limit, your balance transfer cap would be £2,850. This means you could transfer up to £2,850 across one or more balances, as long as the combined amount does not exceed the limit set by the lender.

If the balance you want to transfer is higher than this amount, the lender will process only part of the transfer and leave the remaining balance on your existing card.

If there are any transfer fees, these also need to be taken into consideration.

Mintip: If only part of your balance is transferred, the remaining amount stays on your old card. Make sure you continue making payments to your existing provider until the balance is fully cleared.

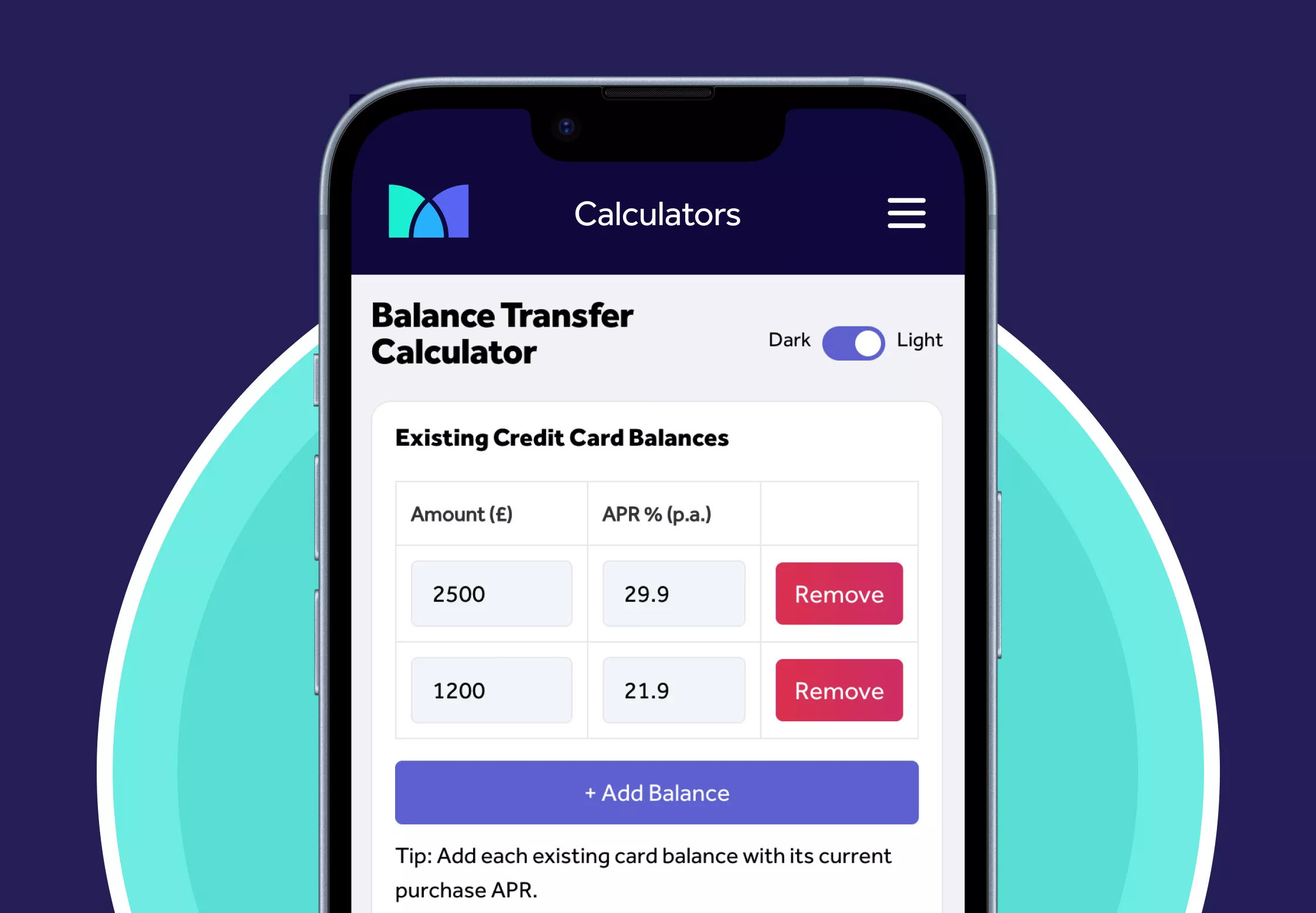

Balance transfer calculator

Before applying for a new balance transfer card, it can help to check how long it may take to repay your balance and whether the transfer limit is likely to be enough for your needs. Using Mintify’s balance transfer calculator gives you a clearer picture of potential repayment times and how much interest you could avoid compared with staying on your current card.

Use our Balance Transfer Calculator to find the right card for you.

If you’re carrying credit card debt, a balance transfer credit card can help you reduce interest costs and repay your balance more efficiently by moving your balance to a new card with 0% interest for a set period. Using a balance transfer calculator helps you understand how much interest you could potentially save by transferring debt from your existing cards to a balance transfer card.

Why your balance transfer limit may be lower than expected

Your balance transfer limit may be lower than expected if the credit limit you are offered on the new card is smaller than anticipated. Because the balance transfer limit is usually a percentage of your credit limit, a lower credit limit reduces the amount you can move.

Other factors can also influence the final limit, including:

- Your income: lenders assess the credit offered against your earnings and overall affordability.

- Existing borrowing: higher levels of debt can result in a more cautious credit limit being set.

- Credit utilisation: using a large proportion of your current credit can reduce how much additional credit is made available.

- Recent credit applications: several applications in a short period can affect the limit you are offered.

These points vary between lenders and form part of their assessment of affordability and risk, so the balance transfer limit you receive may differ from the indicative ranges shown in marketing or comparison tables.

What is my balance transfer limit if I have bad credit?

If you have bad or limited credit, you may still be able to get a balance transfer card, but the credit limit you are offered is likely to be lower than for someone with a stronger credit history. Because the balance transfer limit is usually a percentage of your credit limit, this can reduce the amount you are able to move.

Some lenders offer credit builder balance transfer cards with shorter 0 percent periods or higher fees. These products may reduce the interest you pay compared with staying on a standard credit card rate, depending on how you use the account.

Using an eligibility check can help you see which cards you may be eligible for without affecting your credit score, but it cannot confirm the credit limit or balance transfer limit you will receive.

Important: Once the 0% promotional period ends, the card’s standard interest rate will apply to any remaining balance. This rate is usually higher than the introductory offer, so checking the post-promo APR and ensuring the repayments remain affordable can help you avoid unexpected costs.

Find the right Credit Card for you

No impact to your credit score

Find out which cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Balance transfer rules and restrictions

Balance transfer cards come with specific rules that affect which balances can be moved and how much you are able to transfer. These restrictions vary by lender and product, but commonly include:

- Same banking group restrictions: you usually cannot transfer a balance between cards issued by the same banking group, even if the card brands differ.

- Ineligible account types: some lenders do not accept transfers from store cards, non-UK cards or certain specialist credit products.

- Transfer frequency limits: some cards cap the number of transfers you can make or limit how many can be completed within a single statement period.

- Transfer amount caps: there may be limits on how much can be transferred in one transaction or across the lifetime of the promotional offer.

- Time-limited transfer windows: promotional balance transfer rates are usually only available for a set period after account opening, typically around 60 to 90 days. Transfers made after this window may be charged at the standard rate.

These rules are set by the credit card provider and are shown in the product terms before you complete a transfer. They cannot be overridden during the application process.

What you can do if your balance transfer limit is too low

If your balance transfer limit is lower than the amount you want to move, the lender will process only part of the transfer. In this situation, you can choose which balances to move first, often focusing on the ones with the highest interest rate or the shortest remaining promotional period.

You can also check whether you are eligible for another balance transfer card, although multiple applications in a short period may affect your credit rating. Some users choose to wait for their account to stabilise or for their credit limit to be reviewed by the provider, although limit increases are never guaranteed and depend on the lender’s assessment.

Even if only part of your balance is transferred, moving a portion of your borrowing to a 0 percent promotional period can still reduce the interest you pay compared with leaving the full balance on your existing card.

Important: If you have built up debt that you are finding difficult to manage, it may help to speak with a free and impartial debt advice service before taking on new credit. Support is available from organisations such as StepChange, National Debtline and MoneyHelper.

How your credit score affected by a balance transfer

Taking out a balance transfer card can affect your credit score in several ways. The impact depends on how you manage the account once it is open, as well as how much of your new credit limit you use. Key points include:

- Hard searches: applying for a new card usually leaves a hard search on your credit file, which may cause a small, short-term dip in your score.

- Credit utilisation: moving a balance to a new card can change how much of your total available credit you are using. A lower utilisation ratio can have a positive effect, while higher utilisation may have the opposite impact.

- Payment history: making payments on time is essential. Missing a payment can lead to losing the promotional rate and may harm your credit rating.

- Soft searches: using eligibility checks before applying does not affect your credit score, as these checks are not visible to lenders.

How your score changes will depend on your wider credit profile and how you manage your borrowing after the transfer.

Mintip: Before applying for a new balance transfer card, use a free eligibility check to see which cards you may qualify for without affecting your credit score. This helps you avoid unnecessary hard searches and compare promotional terms more confidently.

Where to find the best balance transfer deals

Balance transfer limits and promotional terms vary between lenders, so it is important to compare the options available before you apply. To see a selection of balance transfer cards in the UK, visit our Top 10 balance transfer credit cards.

Find the right Credit Card for you

No impact to your credit score

Find out which cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Recommended Reading

If you want to explore more balance transfer and credit card topics, these guides may help:

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

What is a balance transfer fee?

How to do a balance transfer on a credit card

Marbles credit card review – is it a good option to consider?

When to do a balance transfer (and how to plan ahead)

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity. Mintify is an Introducer Appointed Representative of Creditec Limited. We provide editorial reviews of the whole market, but we only provide links to apply for products available through Creditec’s panel of lenders. We may earn a commission if you click these links. This does not affect our editorial independence, but it limits the products you can apply for directly on this site.