How to do a balance transfer on a credit card

Editor, Consumer Finance: Michelle Blackmore

Last Updated: February 6, 2026

In This Article

Quick Answer: To do a balance transfer, you give your new card provider the details of the credit card you want to move a balance from. Some providers let you do this during the application and others ask you to do it once the new card is open. The provider then requests the transfer on your behalf. Keep paying your old card until the transfer appears on your new account.

What a balance transfer does

A balance transfer moves existing credit card debt from one provider to another credit card, normally with a different provider.

It does not reduce the amount you owe. Instead, it shifts the balance to another card, sometimes with a promotional interest rate for a set period.

The promotional rate, often 0 percent interest, only applies to the amount you transfer and will change once the offer ends.

Some providers charge a transfer fee and most set limits on how much can be transferred.

A balance transfer will be suitable for some people but not for others, so it is important to check whether it fits your circumstances before applying for new credit.

How to do a balance transfer

A balance transfer is completed by your new credit card provider once your account is open. The steps below outline the general process in the UK. The exact flow can vary between providers, so it is important to check the information for the specific card you are considering.

- Apply for a balance transfer credit card and if you are approved, your new credit card account will be opened. Some providers let you request the balance transfer during the application, while others ask you to do it once the new card is active.

- Give the new provider the details of the card you want to move a balance from. This usually includes the card number and the amount you would like to transfer.

- The new provider will request the balance transfer on your behalf and moves the agreed amount across from your old card to your new card.

- Keep making payments to your old card until the transferred balance appears on your new account statement. This helps you avoid missing a payment while the transfer is being processed.

How the balance is actually moved between card providers

When you request a balance transfer, you do not move the funds yourself. The process is handled directly between the two lenders. Understanding how this works can make the transfer easier to follow and helps you know what to expect once the request is made.

- Your new card provider contacts your existing provider using the card details you supplied. This request is made securely and does not require you to move any money manually.

- Your existing provider confirms the account details and the amount being requested. They will only release up to the value agreed by your new provider.

- The agreed amount is then sent directly from the new provider to the existing provider to pay down the balance. You will not receive the funds yourself.

- Once the payment is processed, your old card balance reduces by the amount transferred and the same amount appears as a new balance on your new card.

- The timing and processing steps can vary slightly between providers, so it can help to check the information supplied with your new card.

In simple terms, your new provider pays the agreed amount to your old provider to reduce your existing balance. The same amount is then added to your new credit card, so you now owe the new provider instead of the old one.

Example: If you have a balance on a Santander credit card and request a balance transfer to a new HSBC credit card, HSBC will send the agreed amount directly to Santander to reduce your existing balance. You will not receive the funds yourself. The same amount will then appear on your HSBC balance transfer card. If fees are charged by HSBC, these will also be added to your overall balance. This example is for illustration only and does not represent any specific product or guarantee any particular outcome.

What to check before you do a balance transfer

Before starting a balance transfer, it helps to look at the key points that can affect the cost and whether the option fits your circumstances. Credit card providesr set different rules, fees and limits, so reviewing the details on the specific card you are considering can make the process clearer.

- The promotional interest rate and when it ends. Promotional rates apply for a set period and will change once the offer expires.

- The balance transfer fee. This is usually a percentage of the amount you move and can affect the total cost of the transfer.

- How much you can transfer. Many providers set limits, often linked to your credit limit once the account is opened.

- Time limited transfer windows: promotional balance transfer rates are typically only available for a set period of time from account opening, typically around 60 to 90 days. Transfers made after this window are usually charged at the standard rate.

- Which providers you can transfer from. Some lenders do not accept transfers from cards within the same banking group.

- How payments are allocated. Spending or cash transactions can attract different interest rates and may not benefit from the promotional period.

Balance transfer fees can catch people out. Some cards have no fee, but if one applies, it is added to your new card balance when the transfer is completed. It is worth checking the fee with your new provider so you know exactly what will appear on your new statement.

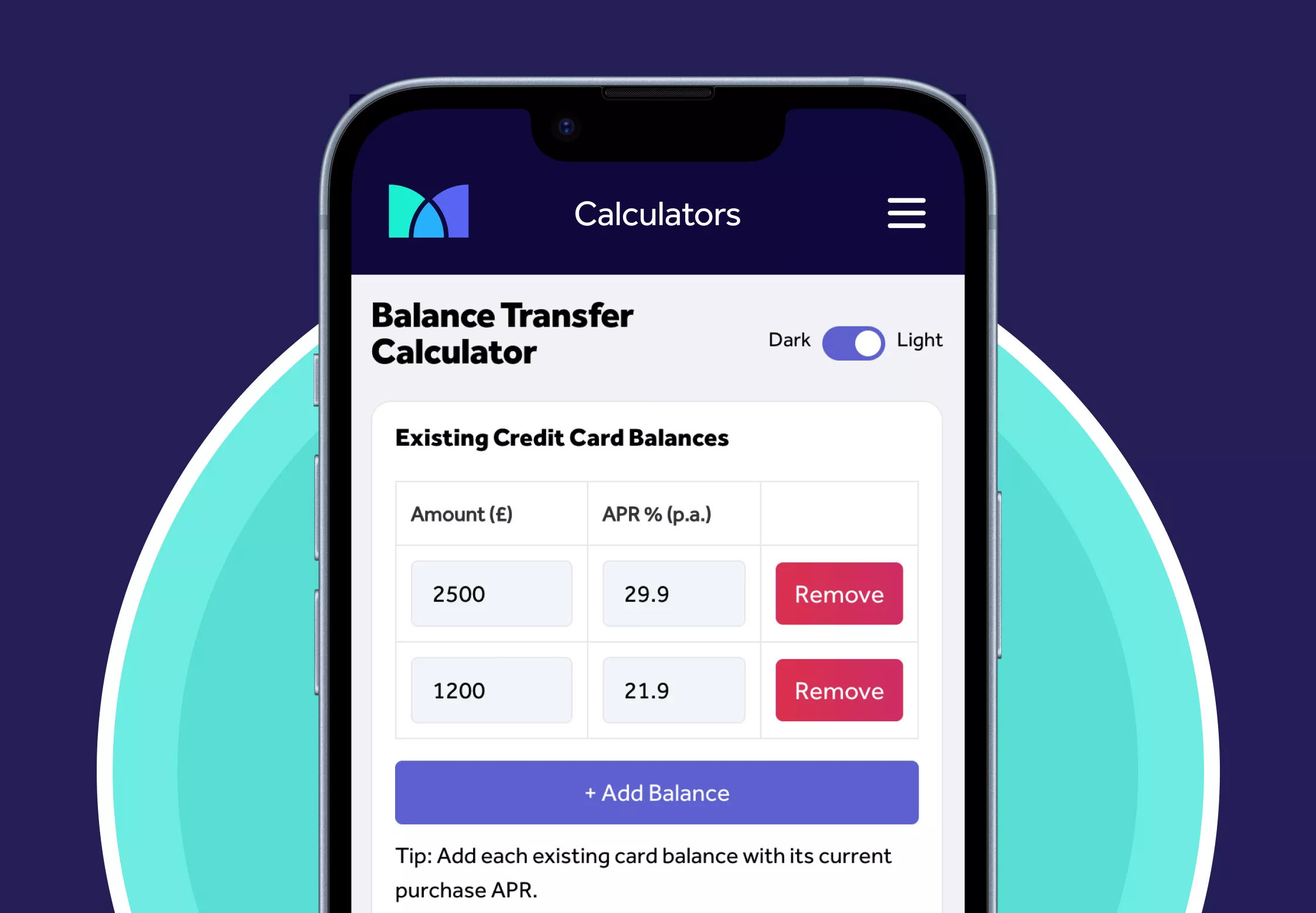

You can use the balance transfer calculator to see how fees and promotional terms could affect the overall amount.

Plan Before You Switch

Use our Balance Transfer Calculator to find the right card for you.

If you’re carrying credit card debt, a balance transfer credit card can help you pay it down faster by moving your balance to a new card with 0% interest for a set period. Using a balance transfer calculator helps you understand how much interest you could potentially save by transferring debt from your existing cards to a balance transfer card.

Risks of balance transfers

Balance transfers can help you manage existing credit card debt, but the option also comes with points to be aware of. Understanding these risks can help you decide whether a balance transfer fits your circumstances and how to manage the new card once the transfer is completed.

- Missing a payment on your new card can lead to the promotional rate ending early. If this happens, the provider will charge the standard interest rate on the remaining balance.

- Using the new card for spending during the promotional period can attract different interest rates and make it harder to keep track of what you owe.

- A balance transfer fee may increase the total balance on your new card. Even a small percentage fee can make a noticeable difference to the amount you owe.

- Promotional periods do not last indefinitely. Once the offer ends, interest is charged at the rate set by the provider.

- Forgetting that balance transfer offers usually have a time window, often only available for around 60 to 90 days after account opening and transfers made later may be charged at the standard rate.

- Some providers do not accept transfers from cards within the same banking group, so the option may not be available for every card.

- Applying for new credit leaves a hard search on your file. Several recent applications can make it harder for some people to access other borrowing.

Mintip: You can check your eligibility for balance transfer cards using a soft search. This does not affect your credit score and helps you see which cards you may be considered for before deciding whether to apply.

When a balance transfer may not be suitable or available as an option

A balance transfer can help in some situations, but it will not suit everyone. The points below outline scenarios where another approach may be more appropriate. This can help you decide whether transferring a balance fits your circumstances before applying for new credit.

- If the amount you want to transfer is small. A transfer fee will increase the balance moved to your new card, and for smaller amounts this can make the overall cost higher than expected. Some balance transfer cards do not charge a fee, but availability varies by provider and individual circumstances.

- If you are finding it hard to make existing repayments. A balance transfer will not reduce the amount you owe and you must still make monthly payments on time. Missed payments can end any promotional rate early, which may increase the cost.

- If your credit file shows recent defaults or several missed payments. Some providers may be less likely to offer a promotional rate in these circumstances.

- If you use your everyday spending. Mixing purchases with a transferred balance can make it harder to track what you owe and may attract different interest rates.

- If you already have several recent credit applications. Another hard search may make it harder for some people to access other borrowing.

- If your current provider is within the same banking group as the new card. Many providers do not allow transfers within the same group, so the option may not be available.

Important: Missing payments can lead to losing the 0% introductory offer and may affect your credit rating. If you’re not sure a balance transfer is the right way to manage your credit card debt, free and impartial support is available from organisations such as StepChange, National Debtline and MoneyHelper.

Alternatives to a balance transfer

A balance transfer is not the only way to manage existing credit card debt. Depending on your circumstances, another option may be more suitable. The points below outline common alternatives and how they differ.

- Speaking with your current provider. They may be able to explain your repayment options or discuss any changes to your existing rate or plan.

- Paying more than the minimum on your current credit card. Increasing your monthly payments reduces your balance faster and can lower the amount of interest charged.

- Using a personal loan to consolidate borrowing. A loan offers fixed monthly repayments over a set term, but interest rates vary and it will not be right for everyone.

- Reviewing your spending and budget. Making small adjustments can sometimes help reduce reliance on credit and support repayment progress.

- Seeking free, impartial guidance. organisations such as StepChange, National Debtline and MoneyHelper can help you understand the options available if you are finding it difficult to keep up with repayments.

Common mistakes to avoid when making a balance transfer

Balance transfers can be useful in some situations, but certain habits or assumptions can make them less effective. Being aware of the points below may help you manage the process more smoothly.

- Stopping payments on your old card too early. Continue to pay it until the transfer appears on your new account to avoid missing a payment.

- Thinking the full balance was transferred when only part of it moved. Providers may limit the amount they accept based on your credit limit or their own rules. If only part of the balance is transferred, you must keep paying your old card until the remaining amount is cleared.

- Using the new card for spending during the promotional period. Spending can attract different interest rates and make it harder to keep track of what you owe.

- Relying only on the promotional period. The rate will change once the offer ends, so it can help to plan how you will manage the balance over time.

- Ignoring the transfer fee. Even a small percentage fee can add to the total cost, so it is helpful to compare the fee with any potential benefit.

Key things to keep in mind when making a balance transfer

The points below summarise what is helpful to understand before, during and after arranging a balance transfer. These can support you in deciding whether the option fits your circumstances.

- Promotional interest rates last for a set period and will change once the offer ends.

- A transfer fee may apply and is normally added to your new card balance when the transfer is processed.

- Balance transfer offers often expire within 60 to 90 days, and transfers made after this window may be charged the standard rate.

- Providers set limits on how much you can move, which may mean only part of your balance is transferred.

- You must keep paying your old card until the balance transfer appears on your new account and the old account shows a £0 balance.

- Avoid using the new card for spending during the promotional period, as different interest rates may apply.

- You can use Mintify’s balance transfer calculator to see how fees and promotional terms could affect the overall amount you will owe.

Take a free credit card eligibility checker to see which balance transfer cards you could be eligible for with no impact on your credit score.

Find the right Credit Card for you

No impact to your credit score

Find out which cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Recommended Reading

If you want to explore more balance transfer and credit card topics, these guides may help:

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

What is a balance transfer fee?

Marbles credit card review – is it a good option to consider?

When to do a balance transfer (and how to plan ahead)

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity. Mintify is an Introducer Appointed Representative of Creditec Limited. We provide editorial reviews of the whole market, but we only provide links to apply for products available through Creditec’s panel of lenders. We may earn a commission if you click these links. This does not affect our editorial independence, but it limits the products you can apply for directly on this site.