No fee credit cards in the UK – balance transfer, cashback and travel options explained

Editor, Consumer Finance: Michelle Blackmore

Last Updated: February 6, 2026

In This Article

Many people look for no annual fee credit cards to help reduce costs. With this type of card, you won’t pay a yearly or monthly account fee simply for holding it. This can make it appealing if you want to keep expenses down, or if you plan to use the card only occasionally.

However, no annual fee does not mean there are no other costs. Interest charges will apply unless you repay your balance in full each month, or you are within a 0% promotional period. Other fees may also apply, for example, balance transfer fees, cash advance charges or foreign transaction costs. Some UK credit card providers offer additional benefits, such as fee-free balance transfers or no foreign transaction charges when spending abroad. These features vary between products and providers.

In this guide, we explain the main types of no annual fee credit cards available in February 2026, including how they work and the situations they may suit. This information is designed to help you compare options and make an informed choice based on your needs and circumstances.

You can also view a full range of no annual fee cards, including those focused on balance transfers, cashback, rewards, and overseas spending, on our no annual fee credit cards comparison. You can check your eligibility for selected cards without affecting your credit score.

What counts as a no fee credit card

A no fee credit card does not charge a fee simply for having the card. Some lenders make this a permanent feature, while others waive the fee for the first year only. This is often offered on cashback or rewards cards as an incentive for new customers to sign up. It can be useful, as it lets you try the card and assess whether it suits your needs without paying an annual fee straight away.

Even if a card has no annual fee, it may still charge other fees, such as balance transfer fees, foreign transaction fees, cash advance fees or late payment charges. Always read the terms offered to you to ensure you understand the full cost of that card.

Hidden fees to watch out for

Even if a credit card has no annual fee, it may still have other costs that can add up over time. Knowing these charges in advance can help you avoid surprises and choose a card that fits your budget.

- Balance transfer fees: even if there is no annual fee, transferring a balance may cost 2 to 3 percent unless the card specifically waives it.

- Foreign transaction fees: typically 2.75 to 2.99 percent unless the card is designed for travel.

- Cash advance fees: charged when withdrawing cash, often at a 3% interest rate and usually there is no 0 percent promotional interest free period.

- Late payment charges: a common amount charged is £12.00 but this can vary per lender. Also, if you miss payments it can also impact/remove any promotional rates.

- Interest rates after the interest-free period: purchases are often interest-free for up to around 56 days if you pay in full. After this, the card’s standard APR applies to any remaining balance which is why it’s important to always try and pay your balance in full each month to avoid paying any interest at all.

No fee balance transfer credit cards

A balance transfer lets you move existing debt from one card to another, often with a 0 percent interest period. Most cards charge a transfer fee of 2 to 3 percent of the amount moved. Some waive this fee, making them “no fee balance transfer” cards.

Example scenario: You have £2,000 on a card at 21.9 percent APR. Moving it to a 0 percent card with no transfer fee and an 18-month interest-free period could save you money, provided you clear the balance before the promotion ends. Once the interest-free period is over, the card’s standard APR will apply to any remaining balance.

Not everyone will be eligible for a balance transfer card without a transfer fee. In some cases, even with a fee, transferring a balance and benefiting from a period of no interest can still be worthwhile if the savings outweigh the upfront cost. Compare all balance transfer options, including cards designed for people with bad credit, in our Top 10 balance transfer credit cards guide.

You can also use Mintify’s Balance Transfer Calculator to enter your own details and see how much you could save with a balance transfer credit card compared with your current card.

Mintip: When a 0% or low-interest promotional period ends, the card’s standard APR will apply to any remaining balance.

Plan Before You Switch

Use our Balance Transfer Calculator to find the right card for you.

If you’re carrying credit card debt, a balance transfer credit card can help you pay it down faster by moving your balance to a new card with 0% interest for a set period. Using a balance transfer calculator helps you understand how much interest you could potentially save by transferring debt from your existing cards to a balance transfer card.

Cashback credit cards with no annual fee

Cashback cards or Rewards cards can give you a percentage of your spending back through points other than actual cash back. Some have no annual fee, which means you can keep them long-term without cost.

Example scenario: You spend £500 a month on everyday purchases and pay the balance in full. A no annual fee cashback card offering 1 percent back would earn you £60 a year without any additional fees for the card itself. For example, if you’re a regular Tesco shopper, Tesco offers a variety of credit cards, including low-interest and balance transfer options, and some with no transfer fee. Many Tesco cards also allow you to earn Tesco points on your spending. This example is for illustration only; other similar products from different providers are available.

No fee credit cards for use abroad

Many UK credit cards charge a foreign transaction fee of around 2.75 to 2.99 percent when used overseas. Some cards remove this charge, making them useful for travel.

Example scenario: You spend £1,000 abroad on a no fee travel card. Without the foreign transaction fee, you save around £27.50 to £29.90 compared to a standard card.

Many travel credit cards charge annual fees because they include premium perks such as air miles, travel insurance, and airport lounge access. For frequent travellers, the value of these benefits can outweigh the cost. However, if you only need a card with no foreign transaction fees, or you have a lower credit score, there are options with no annual fee. For example, the Zopa credit card offers no fees on foreign purchases, making it a useful choice for occasional travellers or those building credit. This example is for illustration only; other similar products from different providers are available.

What’s new in 2026

Credit card features and offers change from time to time, with promotional deals, new rewards structures, and updated terms appearing throughout the year. Taking a free eligibility check can help you see which cards you may qualify for and the latest offers available to you, without affecting your credit score. Some new changes seen are:

- Promotional 0% periods on some no fee balance transfer cards have reached up to 12 months. The length of promotional periods you are offered may be shorter and will depend on your circumstances and the lender’s assessment.

- Some cashback cards now have lower monthly spend requirements to unlock rewards.

- More travel credit cards and even standards credit cards are offering no foreign transaction fees as a standard feature rather than a short-term promotion.

Pros and cons of no fee credit cards

Pros

- Overall borrowing costs are lower and you can keep the card open without any annual fees

- You may still be able to access credit building cards, rewards, cashback or travel benefits

- Many 0% promotional cards for balance transfers or 0% purchase cards are available, including options for people with bad credit.

Cons

- Having an extra card might tempt you into spending more.

- Some offer fewer perks or lower reward rates

- Interest applies if you do not pay in full each month; but this applies to all cards

Myths about no fee credit cards

- Myth: No fee means free to use

- Fact: Interest and other fees may still apply.

- Myth: No annual fee credit cards always have lower costs

- Fact: Some have higher APRs to offset the lack of a fee.

- Myth: All no fee cards are basic

- Fact: Some offer rewards, travel perks or long 0% promotions.

How to choose the right no fee credit card

Selecting the best no fee credit card depends on how you plan to use it. While avoiding an annual fee can save money, it’s still important to compare other features and make sure the card works for your spending habits.

- Decide whether you need it for credit building, balance transfers, rewards or travel

- Check the APR, promotional period length and any additional fees

- Match the card’s features to your typical spending and repayment patterns

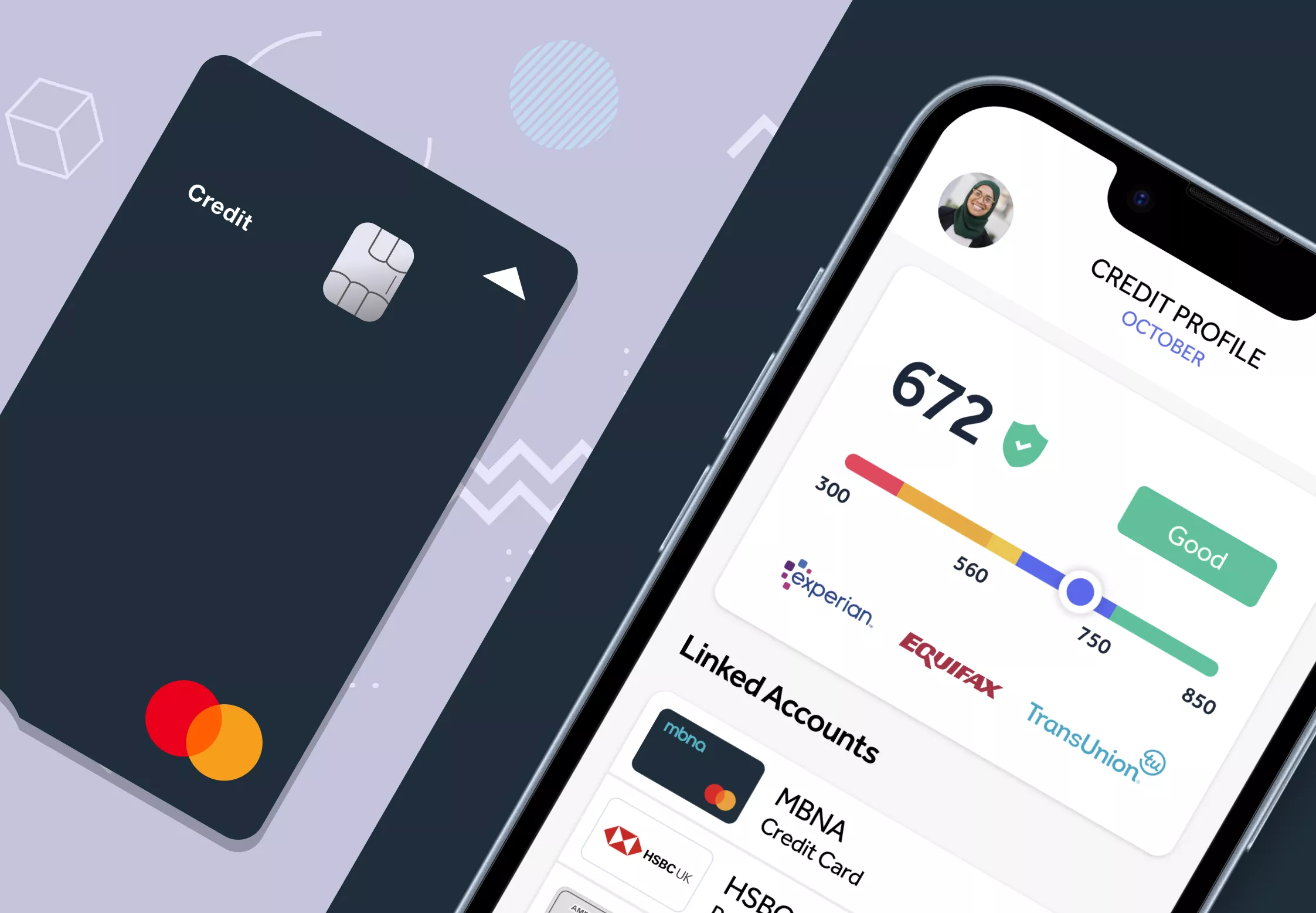

- Use a soft search eligibility checker to see your chances without affecting your credit score

Once you’ve compared your options, take a free eligibility check to see which cards you could be approved for and view the personalised offers without impacting your credit score.

Mintip: Passing an eligibility check is not a guarantee of approval. Final decisions are made by the lender.

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Frequently Asked Questions

What does a no fee credit card mean?

It means the lender does not charge you a yearly or monthly account fee to hold the card. Other charges such as interest or transaction fees may still apply.

What credit cards have no balance transfer fee?

Some UK cards waive the standard 2 to 3 percent balance transfer fee. These offers change often, so check the latest terms before applying. You can check out the Top 10 balance transfer credit cards guide including options for bad credit.

How do cashback credit cards with no annual fee compare?

What credit cards have no foreign transaction fee?

While travel credit cards often include no foreign transaction fees because they are designed for overseas spending, some other cards, such as the Zopa and Zable credit cards, also remove this charge. Always check the card’s terms, as even if foreign transaction fees are waived, there may be other costs such as cash withdrawal charges or a higher APR.

What are the best credit cards with no annual fee?

The best choice depends on your personal needs. Some focus on balance transfers, others on rewards or travel. Compare no annual fee credit card features and fees to find the one you think is right for you.

Final thoughts on no annual fee credit cards

No annual fee credit cards can provide a way to access credit, rewards, or travel perks without paying a yearly account fee. Interest and other charges may still apply, so it’s important to compare the full cost and features before applying. You can view current offers and take a free eligibility check in minutes on our no annual fee credit cards comparison. You can also check your eligibility for free and it will not affect your credit score.

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

What is a balance transfer fee?

How to do a balance transfer on a credit card

Marbles credit card review – is it a good option to consider?

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity