What is a balance transfer fee?

Editor, Consumer Finance: Michelle Blackmore

Last Updated: February 6, 2026

In This Article

Quick Answer: A balance transfer fee is a charge added when you transfer your existing credit card balance to a new balance transfer card. Fees typically range between 1% and 3% of the transfer amount; some lenders also set a minimum charge, usually around £3 to £5, which applies if the percentage fee would be lower.

What is a balance transfer fee and how does it work?

A balance transfer fee is a charge applied when you move an existing credit card balance to a new balance transfer credit card. The fee is added to your new card balance once the transfer is processed. It is normally a percentage of the amount you transfer, although some lenders also set a minimum fee, usually around £3 to £5, if the percentage amount would be lower.

The fee forms part of the overall cost of using a balance transfer card, even when the promotional interest rate is 0 percent. This means your starting balance will be slightly higher than the amount you moved.

Example: If a card charges a 3 percent balance transfer fee with a £3 minimum fee and you transfer £1,300, the percentage fee would be £39. Because this is higher than the £3 minimum fee, the £39 charge applies. Your new starting balance would therefore be £1,339.

Why do balance transfer fees exist?

Lenders apply balance transfer fees to cover the cost of offering long 0 percent introductory periods. During these promotional windows, the lender does not earn interest on the transferred balance, so the fee helps offset the risk and funding cost.

Cards with higher fees often come with longer promotional periods, while cards with low or no fees typically offer shorter interest free terms. The fee is essentially part of the pricing structure that allows lenders to provide interest free borrowing for a set time.

Do all balance transfer cards charge a fee?

Not all balance transfer cards charge a fee. Some products offer no fee transfers, where you pay only the amount you move. These cards can be useful if you want to avoid upfront costs, but they often come with shorter promotional periods.

Cards that do charge a fee usually offer longer 0 percent terms or wider eligibility bands. Checking the summary box on the product page helps you understand the exact fee and promotional period before you apply.

Comparing no fee balance transfer cards

Some balance transfer cards do not charge a balance transfer fee, which means you only repay the amount you move across. These cards can reduce the upfront cost of switching, but the promotional period and eligibility criteria vary between credit card providers. The comparison below shows how two no fee options differ so you can understand what each offers before you apply. There are other credit cards on the market that may not appear here but could suit you better, depending on how much you need to transfer and what you value most.

Santander Everyday No Balance Transfer Fee |  Barclaycard Platinum No Fee Balance Transfer | |

|---|---|---|

| Account Fee | £0 | £0 |

| Representative APR | 24.90% | 24.90% |

| Purchases Description | 0% for up to 3 months, then 24.90% (variable) p.a. | 0% for up to 3 months, then 24.90% (variable) p.a. |

| Purchases Interest Free | 56 days | 56 days |

| Balance Transfers | 0% for 12 months, then 24.90% (variable) p.a. (0% fee for 12 months) | 0% for 14 months, then 24.90% (variable) p.a. No transfer fees. |

| Incentive on Opening | Benefit from 0% interest on balance transfers and no transfer fee for 12 months with this credit card | No transfer fees, 0% interest on balance transfer for up to 14 months |

| Cashback/Rewards (if applicable) | No cashback scheme | No cashback scheme |

| Minimum Credit Limit | £500.00 | £50.00 |

| Intro Balance Transfers Fee | 0.00% | 0.00% |

| Balance Transfers Fee | 3.00% | 0.00% |

| Foreign Usage (EU) | 2.95% | 2.99% |

| Foreign Usage World | 2.95% | 2.99% |

Credit card providers may change or withdraw their no fee offers at any time, so it is important to check the terms available to you before applying. Taking a free credit card eligibility check gives you an indication of which balance transfer cards you may qualify for, without affecting your credit score. It does not guarantee approval, but it can help you avoid unnecessary hard searches.

Comparing no fee balance transfer cards

Some balance transfer cards do not charge a balance transfer fee, which means you only repay the amount you move across. These cards can reduce the upfront cost of switching, but the promotional period and eligibility criteria vary between credit card providers. The comparison below shows how two no fee options differ so you can understand what each offers before you apply. There are other credit cards on the market that may not appear here but could suit you better, depending on how much you need to transfer and what you value most.

Santander Everyday No Balance Transfer Fee | Barclaycard Platinum No Fee Balance Transfer | |

|---|---|---|

| Account Fee | £0 | £0 |

| Representative APR | 24.90% | 24.90% |

| Purchases Description | 0% for up to 3 months, then 24.90% (variable) p.a. | 0% for up to 3 months, then 24.90% (variable) p.a. |

| Purchases Interest Free | 56 days | 56 days |

| Balance Transfers | 0% for 12 months, then 24.90% (variable) p.a. (0% fee for 12 months) | 0% for 14 months, then 24.90% (variable) p.a. No transfer fees. |

| Incentive on Opening | Benefit from 0% interest on balance transfers and no transfer fee for 12 months with this credit card | No transfer fees, 0% interest on balance transfer for up to 14 months |

| Cashback/Rewards (if applicable) | No cashback scheme | No cashback scheme |

| Minimum Credit Limit | £500.00 | £50.00 |

| Intro Balance Transfers Fee | 0.00% | 0.00% |

| Balance Transfers Fee | 3.00% | 0.00% |

| Foreign Usage (EU) | 2.95% | 2.99% |

| Foreign Usage World | 2.95% | 2.99% |

Credit card providers may change or withdraw their no fee offers at any time, so it is important to check the terms available to you before applying. Taking a free eligibility check gives you an indication of which balance transfer cards you may qualify for, without affecting your credit score. It does not guarantee approval, but it can help you avoid unnecessary hard searches.

Find the right Credit Card for you

No impact to your credit score

Find out which cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Low fee balance transfer cards

Low fee balance transfer cards sit between no fee transfer fee cards and higher fee cards that usually offer the longest promotional periods. These low fee balance transfer cards usually charge around 1 percent to 2 percent to move your balance, which keeps the initial cost low while still giving you access to competitive 0 percent terms.

If you do not qualify for a no fee offer, a low fee card may still lower the upfront cost compared to staying on your existing credit card rate. The value depends on how quickly you plan to repay the balance and the terms you are offered.

The two examples below show how low fee cards differ in terms of promotional length, eligibility, and the fee applied. Other credit cards are available that do not appear in this list. Based on your situation and preferences, a different product may be more suitable.

Bank of Scotland Platinum Low Fee 0% Balance Transfer |  Tesco Bank Low Fee Balance Transfer | |

|---|---|---|

| Account Fee | £0 | £0 |

| Representative APR | 24.90% | 24.90% |

| Purchases Description | 0% for up to 6 months, then 24.90% (variable) p.a. | 24.9% (variable) p.a. |

| Purchases Interest Free | 56 days | 56 days |

| Balance Transfers | 0% for 22 months then 24.94% (variable) p.a. (1.99% fee for 3 months) | 0% for 15 months, then 24.94% (variable) p.a. (0.75% fee) |

| Incentive on Opening | None | When you earn points, you can exchange them for vouchers to save on groceries and fuel or you can get twice the value when using them with Tesco Reward Partners. |

| Cashback/Rewards (if applicable) | No cashback scheme | 5 points per £4 spent (£4 minimum) in Tesco, 1 point for every £4 spent on Tesco fuel (excluding Esso) plus 1 point per £8 spent (£8 minimum) outside Tesco. Must have available credit to earn points. Points are converted to Tesco vouchers or can be exchanged for Partner rewards to receive money off a variety of restaurants, entertainment or Avios points. |

| Minimum Credit Limit | £0.00 | £100.00 |

| Intro Balance Transfers Fee | 1.99% | 0.75% |

| Balance Transfers Fee | 5.00% | 0.75% |

| Foreign Usage (EU) | 2.95% | 2.75% |

| Foreign Usage World | 2.95% | 2.75% |

Card providers may change or withdraw their low fee offers at any time, so it is important to check the terms available to you before you apply for a balance transfer credit card..

Credit builder balance transfer cards

Some lenders offer balance transfer cards designed for people with limited or developing credit histories. These credit builder cards usually have shorter 0 percent periods or higher fees, but they can still reduce your interest costs compared with staying on a standard credit card rate.

They can be useful if you do not meet the criteria for mainstream balance transfer cards. Making payments on time and keeping your balance under control may help improve your credit card eligibility over time, although this is not guaranteed.

Important: Missing payments can lead to losing the 0% introductory offer and may affect your credit rating. If you’re not sure a balance transfer is the right way to manage your credit card debt, free and impartial support is available from organisations such as StepChange, National Debtline and MoneyHelper.

Are balance transfer fees worth it?

Whether a balance transfer fee is worth paying depends on how much you can save during the promotional period. A fee can still offer good value if the 0 percent term is long enough for you to repay your balance, as the interest you avoid may be greater than the upfront cost.

If you expect to repay the balance sooner, a no fee or low fee card may work better. The best way to judge this is to look at the total cost rather than the fee alone. This includes the length of the promotional period, the fee charged, and the interest rate that applies once the offer ends.

Balance transfer fees can catch people out. Some cards have no fee, but if one applies, it is added to your new card balance when the transfer is completed. It is worth checking the fee with your new credit card provider so you know exactly what will appear on your new statement.

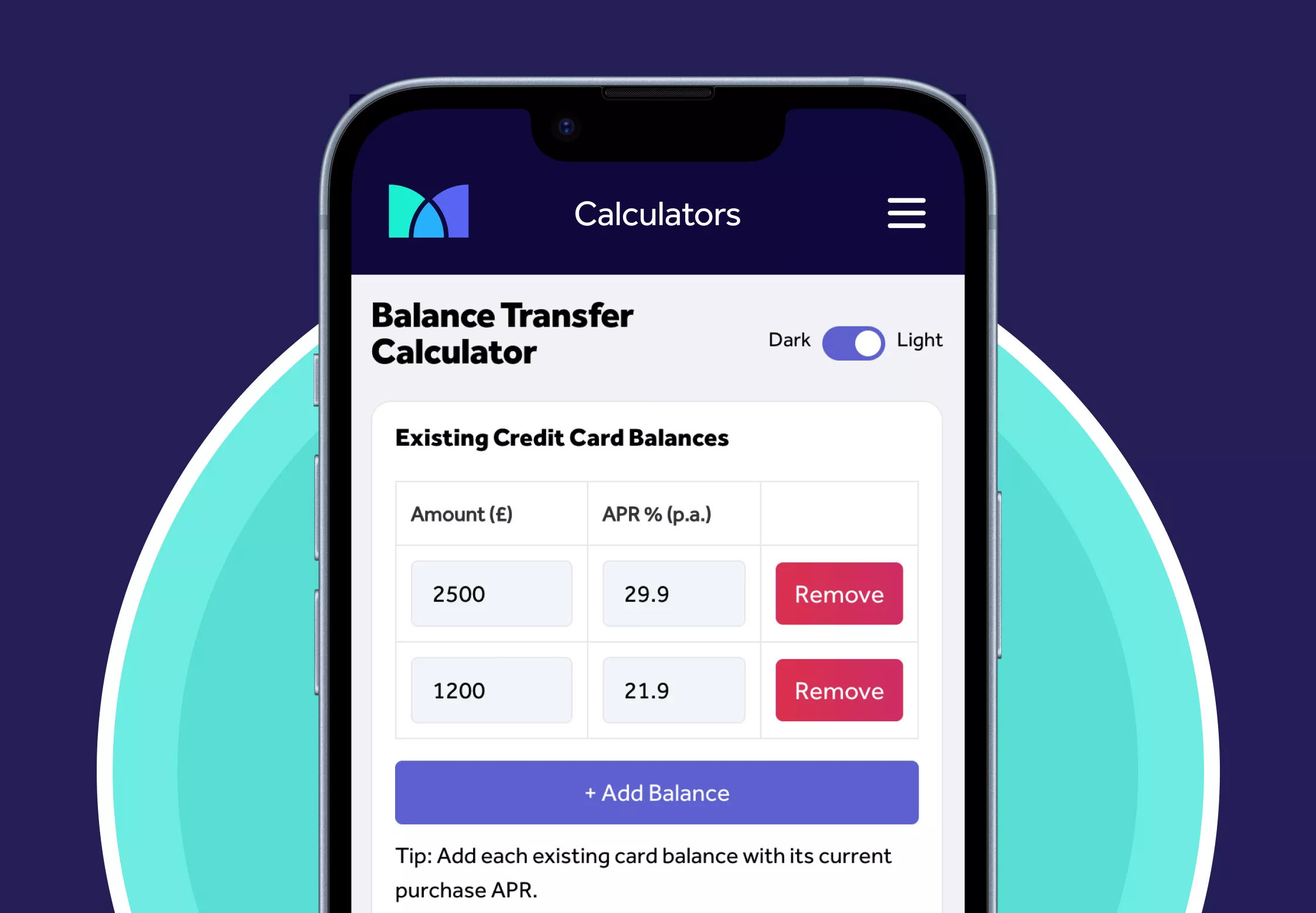

You can use Mintify’s balance transfer calculator to estimate how long it may take to clear your balance and understand how the fee affects your total cost. This helps you compare offers more accurately before you apply.

Plan Before You Switch

Use our Balance Transfer Calculator to find the right card for you.

If you’re carrying credit card debt, a balance transfer credit card can help you pay it down faster by moving your balance to a new card with 0% interest for a set period. Using a balance transfer calculator helps you understand how much interest you could potentially save by transferring debt from your existing cards to a balance transfer card.

Mintip: Check that the repayments will be affordable throughout the promotional period. Missing a payment may end the 0% offer and could affect your credit rating.

When is the balance transfer fee is charged?

The balance transfer fee is applied as soon as your transfer is processed. It is not paid separately. Instead, the fee is added to your new card balance, so your starting balance will include both the amount you transferred and the fee.

The fee follows the same promotional treatment as the rest of the transferred balance, unless the lender states otherwise. This is why your confirmed starting balance may be slightly higher than the amount you originally moved across.

What affects the balance transfer fee?

The balance transfer fee you receive depends on several factors set by the lender and the product. Key points include:

- Promotional period: longer 0 percent terms usually come with higher fees, while shorter terms may offer lower or no fees.

- Credit profile: applicants with stronger credit histories may be offered more competitive fee levels, depending on the lender.

- Minimum fees: many lenders apply a minimum charge, often around £3 to £5, which affects smaller transfers.

- Transfer amount: the percentage fee is applied to the balance you move, so larger transfers result in a higher total fee.

- Product type: some cards, including credit builder balance transfer cards, have higher fees or shorter promotional periods due to different risk profiles.

Mintip: Balance transfer offers are often only available for a short period after you open the account, typically around 60 to 90 days. If you complete the transfer after this window, the standard rate may apply so check the terms you have been offered.

Where can I find the best balance transfer deals?

Balance transfer fees and promotional periods vary between lenders, so it is important to compare offers before you apply. To read more about balance transfer cards, visit our Top 10 balance transfer credit cards. The information is based on promotional terms available at the time of publication.

Find the right Credit Card for you

No impact to your credit score

Find out which cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Recommended Reading

If you want to explore more balance transfer and credit card topics, these guides may help:

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

How to do a balance transfer on a credit card

Marbles credit card review – is it a good option to consider?

When to do a balance transfer (and how to plan ahead)

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity. Mintify is an Introducer Appointed Representative of Creditec Limited. We provide editorial reviews of the whole market, but we only provide links to apply for products available through Creditec’s panel of lenders. We may earn a commission if you click these links. This does not affect our editorial independence, but it limits the products you can apply for directly on this site.