What is a good credit score in the UK?

Editor, Personal Finance: Michelle Blackmore

Last Updated: February 15, 2026

In This Article

Understanding how credit scoring works is an important step in managing your financial wellbeing. At Mintify, we simplify complex financial concepts so you can make confident, informed choices. In the UK, your credit score helps lenders assess how reliably you manage borrowed money and can influence applications for personal loans, credit cards, mortgages, and even some rental agreements.

What does a credit score mean?

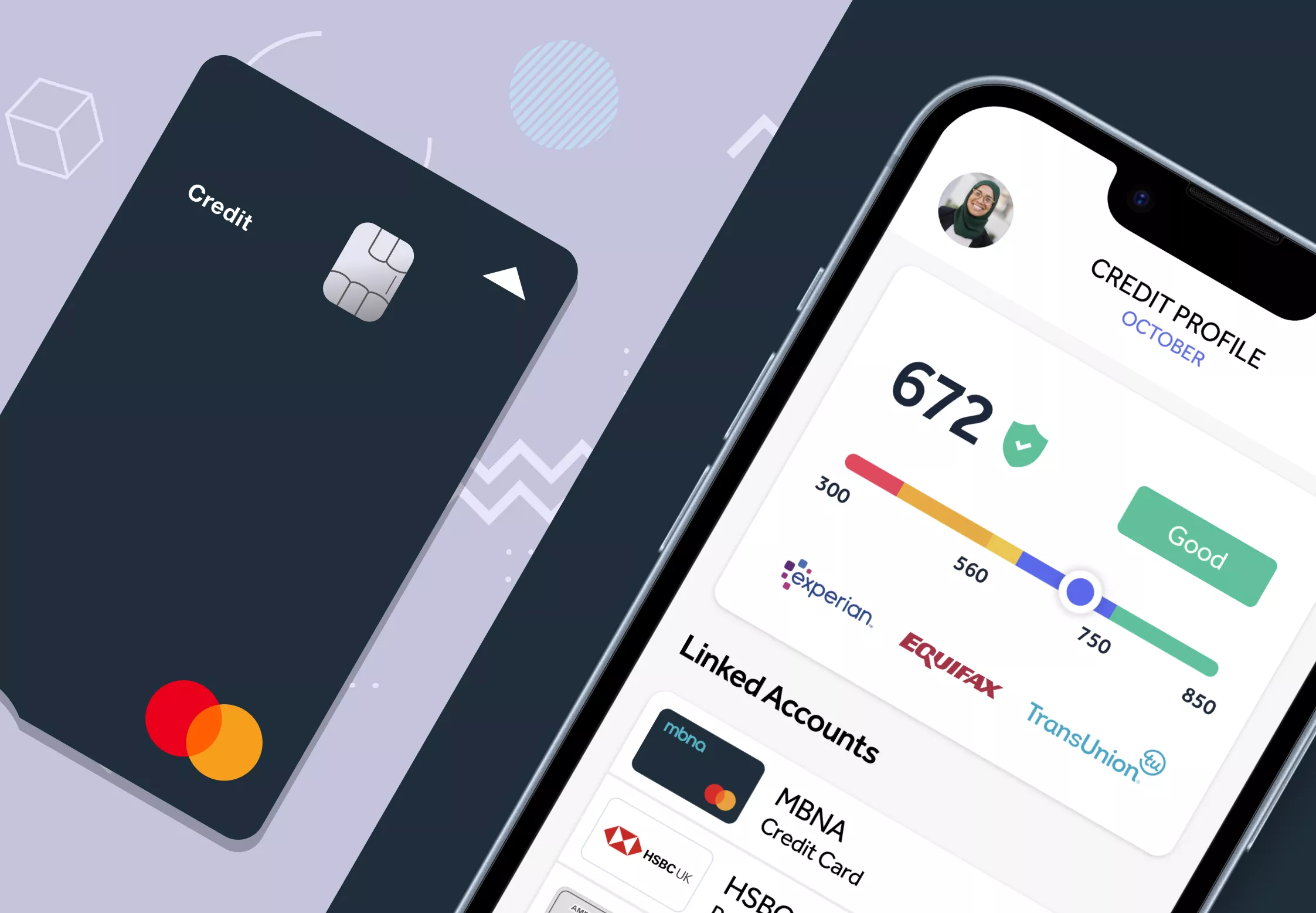

A credit score is a summary of your borrowing behaviour. Think of it as a way for lenders to gauge how likely you are to repay on time. It’s built from information in your credit file, such as payment history, outstanding balances, and the length of your credit accounts. There’s no single “UK credit score”; each agency and lender has its own scoring model, so the number you see may differ depending on where you check.

What is considered a good credit score in the UK?

A good credit score generally means you’re seen as a dependable borrower. There isn’t one exact number that defines it, because every credit reference agency uses a different scale and each lender applies its own assessment criteria. Broadly speaking, a good score signals consistent repayment behaviour, responsible use of credit, and stable financial habits.

Lenders often view this as lower risk, which may improve your chances of being accepted for mainstream credit products including cashback and rewards cards or offered better rates for personal loans.

Mintip: If you’re aiming to strengthen your credit profile, read our guide on 9 habits to improve credit card eligibility. It explains practical ways to build stability and improve your chances of approval for future credit.

What is considered a low or bad credit score in the UK?

A low or “bad” credit score suggests you may have had difficulty managing credit in the past, such as missed or late payments, or limited credit history. It doesn’t mean you can’t borrow, but lenders may view you as higher risk and could offer smaller limits or higher interest rates. The good news is that scores change over time so steady, positive habits can help you move into stronger ranges and access better financial options.

If you are trying to rebuild your credit score, you might want to consider credit builder cards. Our guide on best credit builder cards to build credit could help you understand how these work and some options available, subject to lender approval.

How do lenders decide which rates to offer?

There’s no universal score that guarantees approval. Each lender has its own way of evaluating applications, considering factors like income, employment, existing debts, and repayment history. You might meet the criteria for one provider but not another. That’s why it’s important to check your credit report and use a free eligibility checker before applying. It helps you understand where you stand and reduces the risk of unnecessary hard searches on your file.

How to achieve and maintain a good credit score

Improving your credit score is definitely possible with a bit of time, effort and patience. Here are some practical steps and tips to improve your score:

- Register on the electoral roll: Ensure you’re registered at your current address. This helps companies confirm your identity and increases your credibility.

- Build a credit history: If you have little or no credit history, it can be challenging for companies to assess your reliability, which could lead you to be given a lower credit score. Start small, such as using a credit card responsibly for everyday purchases, pay in full each month and start to establish a credit history.

- Pay on time and in full: Always pay your balances by the due date and, if possible, in full. This demonstrates to lenders your ability to responsibly use credit.

- Keep credit utilisation low: Aim to only use a small portion of your available credit. For example, if your credit limit is £3,000 and you’ve used £1,500, your credit utilisation is 50%. Lowering this to 25% or less can positively impact your score.

What is a good score in the UK to buy a house?

There isn’t a single number that guarantees mortgage approval. Each lender calculates its own internal score when you apply. A higher credit score usually strengthens your application, but affordability, income stability, and deposit size all play major roles. If your score is average or low, improving your overall profile before applying can increase your chances of success.

How do I check my credit score?

You can check your score for free with major credit reference agencies such as Experian, Equifax, or TransUnion. Third-party platforms like ClearScore and Credit Karma also provide free access and regular updates. Checking your own report counts as a soft search and won’t affect your score.

Can I improve my credit score?

To improve your credit score over time, focus on consistent, responsible credit use. Pay bills promptly, reduce outstanding balances, and avoid applying for too many products at once. Responsible management, not quick fixes, is what drives lasting improvement.

Mintip: When selecting a credit card, remember that paying off the full balance each month helps you avoid interest charges.

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited and is acting as a credit broker, not a lender.

Frequently asked questions

To improve your credit score over time, focus on consistent, responsible credit use. Pay bills promptly, reduce outstanding balances, and avoid applying for too many products at once. Responsible management, not quick fixes, is what drives lasting improvement.

What is a good score in the UK out of 1000?

A good credit score means lenders are likely to view you as a reliable borrower. Each credit reference agency uses a different scale, so there isn’t a single “good” number. In general, a higher score reflects positive financial habits, such as making payments on time and keeping balances low, which can help improve your chances of being approved for credit.

Does having a good score guarantee approval?

No. A good score can strengthen your application, but each lender makes its own decision based on affordability, income, and other factors. Even people with high scores may be declined if a lender’s specific criteria aren’t met.

Why is my credit score going down?

Your credit score can fall for several reasons — for example, missed or late payments, high credit utilisation, or multiple new credit applications in a short time. Closing long-held accounts can also shorten your credit history and temporarily lower your score.

Can checking my score lower it?

No. Checking your own credit score counts as a soft search, which isn’t visible to lenders and has no impact on your score or eligibility.

How long do hard searches stay on my file?

Hard searches usually remain visible on your credit report for around 12 months. Their effect on your score reduces over time as you continue to manage credit responsibly.

Can I rebuild from a poor score?

Yes. Credit scores are dynamic and change with your behaviour. Paying bills on time, keeping balances low, and maintaining stability in your accounts can all help you move from a poor score toward a stronger credit position.

Conclusion: Stay informed and build long-term credit health

Understanding how your credit score works and what influences it helps you make confident, informed financial decisions. A strong score develops over time through consistent repayment, low credit use, and responsible borrowing.

Before applying for credit, check your report regularly, use free eligibility tools to understand your options, and always read the terms carefully. Small, steady improvements can make a meaningful difference to your borrowing choices and costs over the long term.

Use eligibility checkers for credit cards and personal loans so you can understand which products you could be eligible for without any impact on your credit file and then be able to choose products that align with your circumstances. Remember, these checks never guarantee approval, but the aim is to help you navigate credit clearly and responsibly.

Mintip: If you’re finding it difficult to manage existing credit or debt, free and impartial help is available from organisations such as StepChange and MoneyHelper. Speaking to them early can help you understand your options and avoid further financial pressure.

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

What is a balance transfer fee?

How to do a balance transfer on a credit card

Marbles credit card review – is it a good option to consider?

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity