What credit score is needed for car finance in the UK?

Editor, Consumer Finance: Michelle Blackmore

Last Updated: February 6, 2026

In This Article

Quick Answer: There is no fixed credit score required for car finance in the UK. Each lender uses its own criteria, and decisions are based on your overall credit history, affordability, income and existing commitments. Check your eligibility to see which products may be considered for you, without affecting your credit score.

Knowing what credit score is needed for car finance in the UK is a common question, particularly as eligibility can feel unclear and different lenders use their own criteria. There is no single score that guarantees approval, which can make the process seem confusing if you are checking your credit file for guidance.

Credit reference agency scores are useful indicators, but they are only one part of the assessment. Lenders also consider your income, existing commitments, payment history and how affordable the agreement is for you.

This guide explains how credit scores are used in car finance decisions, what lenders typically look for, and why your overall financial profile often matters more than the number you see on your file.

You will also find links to related Mintify guides, including how car finance compares with a personal loan and what a good credit score looks like in the UK, so you can review everything in one place before moving forward. All information follows our editorial guidelines, which ensure that the information is clear and based on independent research.

Do you need a specific credit score for car finance?

There is no set credit score required for car finance in the UK. Each lender uses its own underwriting criteria, and decisions are based on your overall financial profile rather than a single number from a credit reference agency. This means two people with similar scores can receive different outcomes depending on their income, existing commitments and recent credit behaviour.

Credit scores from agencies such as Experian, Equifax and TransUnion are helpful for understanding how your credit file is viewed in general, but they are not used as strict pass or fail thresholds. Lenders focus on affordability, your record of repaying previous borrowing, and whether the agreement fits comfortably within your current financial situation.

If you want a broader understanding of how UK credit scores work and what different ranges mean, you can read our guide on what is considered a good credit score in the UK.

How lenders assess your car finance application

When reviewing a car finance application, lenders look at a range of factors to understand whether the agreement is affordable and manageable for you. Credit scores form part of this assessment, but they are not the only consideration. Each lender or broker panel applies its own criteria, which means outcomes can vary between loan providers.

- Income and stability: Lenders check that your income is consistent and sufficient to support the repayments.

- Existing credit commitments: Other loans, credit cards and regular outgoings are reviewed to understand your overall financial position.

- Payment history: A track record of paying on time can be helpful, while missed or late payments may affect the terms you are offered.

- Credit utilisation: How much of your available credit you are currently using can influence how lenders view your borrowing behaviour.

- Length of credit history: A longer, well-managed credit record can provide more evidence of how you handle credit over time.

- Recent applications: Multiple applications in a short period may indicate financial pressure, so lenders will consider this as part of their assessment.

- Type of finance: HP and PCP are assessed slightly differently, particularly where balloon payments or mileage agreements apply.

We have an editorial review of Autolend if you want to understand how one direct lender structures its assessments.

How long do car finance checks take?

Car finance checks can vary between lenders. Some decisions are made quickly once the soft search and affordability assessment are complete, while others may take longer if additional information is needed. Ensuring your details are accurate and up to date can help the process run more smoothly, but each lender follows its own checks and timelines.

If you want to understand the practical steps involved in arranging car finance and how the process works when you need it organised quickly, our quick car finance guide explains what lenders look for, the documents you may need and how to prepare so the application process goes smoothly.

Get Personalised Loan Rates

Find lenders that may be able to approve you

Options for all credit backgrounds

Representative 32.9% APR

No impact to your credit score

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Typical credit score ranges for car finance in the UK

There is no universal score that guarantees car finance approval, and lenders do not all use the same scoring systems. However, credit reference agency ranges can give you a general sense of how your credit profile may be viewed. Higher scores usually indicate a stronger repayment history, while lower scores may reflect missed payments or limited credit experience.

It is important to remember that these ranges are only guidelines. A lender may still offer finance to someone with a lower score if the overall application is affordable, and someone with a higher score may be declined if their circumstances do not meet the lender’s criteria. Each decision depends on the full picture rather than a single number.

One example of how credit agencies categorise scores is from Experian. In autumn 2025, Experian updated its credit score bands to better reflect how lenders were using its scores in practice. These bands can be useful for understanding how your credit file may be viewed, but they do not guarantee approval for any finance product.

| Score Bands (0–1250) |

What This Means |

|---|---|

| ‘Excellent’ 1121 – 1250 |

You may find that more products are visible to you, but approval is not guaranteed. |

| ‘Very Good’ 1001 – 1120 |

You may be shown a broad range of products, although interest rates could vary. |

| ‘Good’ 861 – 1000 |

You may have access to a broad range of products, though interest rates could be higher than those offered to higher-rated profiles. |

| ‘Fair’ 641 – 860 |

You may see fewer products available to you, and some may come with higher rates or limits. |

| ‘Low’ 0 – 640 |

It may be more difficult to be approved and interest rates could be higher. These scores can improve over time with consistent repayment behaviour. |

The table above shows how Experian classifies different score bands and the likely implications for lending. Even if your score falls into a lower band, lenders may still consider your application if the agreement is affordable and meets their wider criteria.

Can you get car finance with bad credit?

Having a lower credit score or previous credit issues does not automatically rule out car finance, but it can make the process more limited and more expensive. Some lenders and broker panels may consider applications from customers with adverse credit, but they will still carry out checks to make sure the agreement is affordable and fits within their criteria.

You may find that any offers you receive come with higher interest rates, a requirement for a larger deposit or shorter terms than those available to customers with stronger credit histories. In some cases, a lender may decide that finance is not appropriate if the repayments would put too much pressure on your budget.

- Some lenders may review applications that include missed payments, defaults or county court judgments, but this varies by provider and is not guaranteed.

- Any offer you receive is likely to depend heavily on affordability, including your income, regular outgoings and existing borrowing.

- Higher APRs, lower borrowing limits or stricter conditions may apply compared with products aimed at customers with stronger credit profiles.

- Making multiple full applications in a short period can make it harder to be approved, which is why soft search tools are often used first.

If you are unsure whether further borrowing is right for you because of existing debts or payment pressures, it can help to take a step back and review your wider finances before applying.

Important: Missing payments can lead to extra charges and may affect your credit rating. Only take out credit if you’re confident you can keep up with the repayments. If your repayments ever become difficult to manage, free and impartial support is available from organisations such as StepChange, National Debtline and MoneyHelper.

How to strengthen your car finance application

There is no guaranteed way to be approved for car finance, but there are steps that can improve your eligibility and help make your overall financial profile clearer and more consistent before you apply. These actions do not raise your credit score automatically, but they can help lenders build a more accurate picture of your circumstances when assessing affordability.

- Check your credit file with all three agencies: Experian, Equifax and TransUnion may hold different information, so it helps to make sure the details are correct and up to date.

- Keep existing credit accounts in good order: Making payments on time and staying within agreed limits can help demonstrate stable borrowing behaviour.

- Reduce outstanding balances where possible: Lower utilisation across credit cards and overdrafts can help improve your overall affordability.

- Avoid multiple applications close together: Several hard searches in a short period can make it harder for lenders to assess your current position.

- Make sure personal details are consistent: Differences in addresses or employment information across accounts can delay or complicate assessments.

- Register on the electoral roll if you are eligible: This helps lenders verify your identity more easily during checks.

If you want to understand how other borrowing structures work outside of HP or PCP, you can read our overview of monthly instalment loans to understand how fixed-term borrowing works.

What if you have no credit history?

Having no credit history can make car finance assessments more difficult because there is less information available to show how you have managed borrowing in the past. This is often described as having a “thin file”. Lenders may take a cautious approach in these cases, focusing more heavily on income stability and whether the agreement is affordable.

Some lenders or broker panels may still consider applications from customers with limited credit history, but the terms offered can vary. You may find that a larger deposit, shorter term or higher interest rate is required to reflect the reduced information available.

- Limited information: With fewer accounts on your file, lenders have less evidence of repayment behaviour.

- Affordability becomes central: Income and regular outgoings play a major role in assessing whether the agreement is manageable.

- Soft searches are helpful: These checks allow you to see which products you may be considered for without affecting your credit score.

- Credit history can build over time: Small, well-managed accounts can help establish a longer-term credit record.

How soft search eligibility checks help

Soft search tools are commonly used in car finance because they allow you to see which products you may be considered for without leaving a mark on your credit file. These free eligibility checkers use a limited version of your credit information, along with details about your income and outgoings, to give lenders an initial view of your circumstances.

A soft search does not show other lenders that you have made an application, and it does not affect your credit score. It is designed to help you understand whether a product might be suitable to explore further before deciding whether to proceed with a full application.

- No impact on your credit score: Soft searches do not appear on your file in a way that affects future lending decisions.

- Helps avoid unnecessary applications: Soft searches give an early view of which products a lender or broker may review further, without affecting your credit score.

- Useful when comparing options: Many broker panels use soft checks to show you the types of products that might align with your circumstances.

- Supports affordability reviews: Lenders can assess your basic financial position without committing to a full credit check.

A soft search does not guarantee that you will be offered car finance, and you should only continue to a full application if you feel the repayments fit comfortably within your wider budget.

Get Personalised Loan Rates

Find lenders that may be able to approve you

Options for all credit backgrounds

Representative 32.9% APR

No impact to your credit score

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Key takeaways: credit scores and car finance

Understanding how credit scores affect car finance can help you prepare before applying, but no single number guarantees an outcome. Lenders look at your wider financial position, including affordability, income stability and your overall credit history, rather than relying on a fixed score threshold.

- There is no set credit score required for car finance in the UK, and each lender uses its own criteria.

- Credit scores are indicators, not pass or fail markers, and lenders consider your full financial profile.

- Affordability checks play a central role in determining whether an agreement is manageable.

- Soft searches can help you understand whether a product may be considered for you without affecting your credit score.

- Your credit file may still be acceptable for some lenders even if it contains limited history or previous issues.

- It can be helpful to review your budget and repayment comfort before deciding whether to proceed with a full application.

If you want to see which types of products may be reviewed for you, you can use a free soft search eligibility check which has no impact on your credit score.

Related Articles

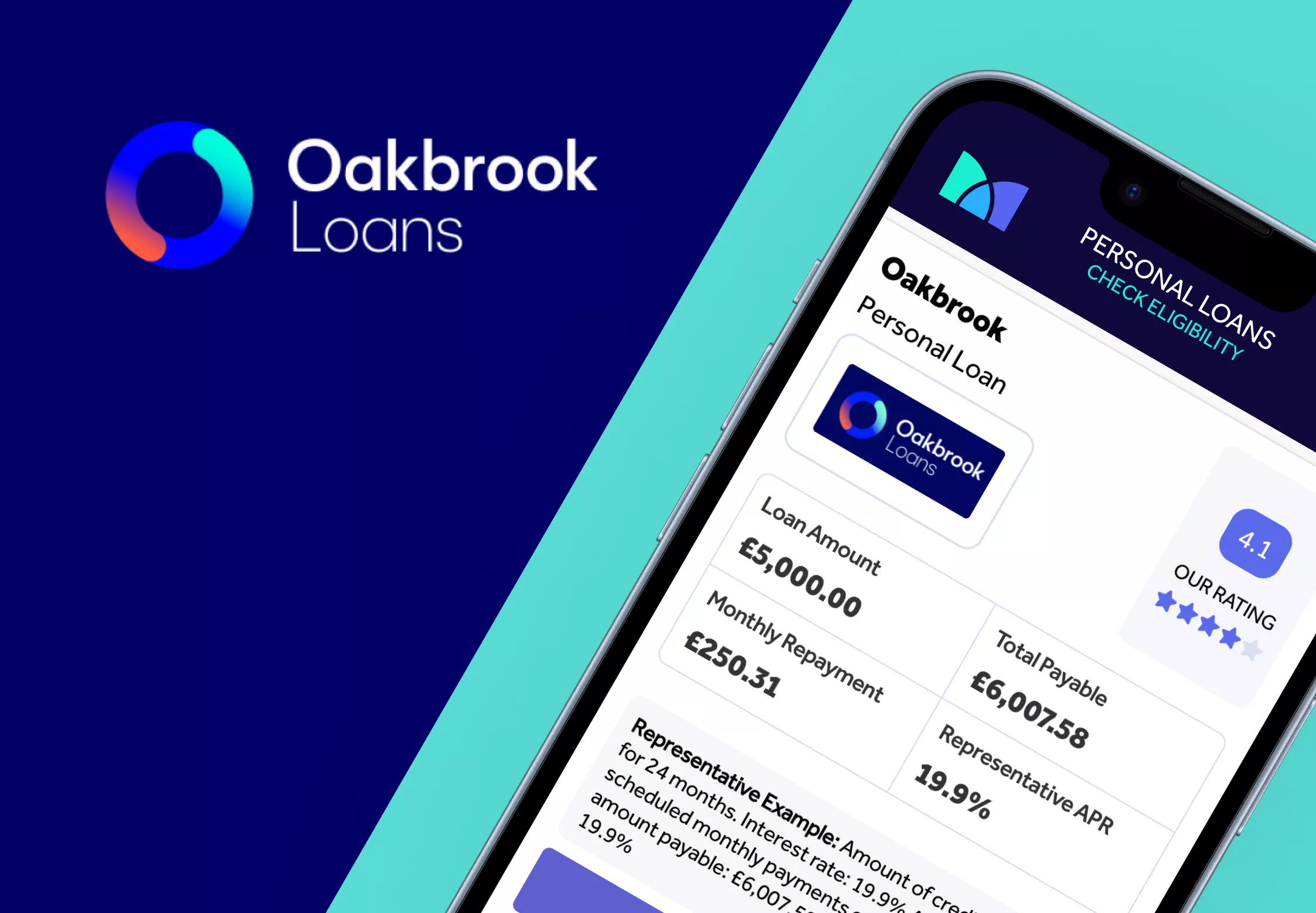

Oakbrook Loans Review

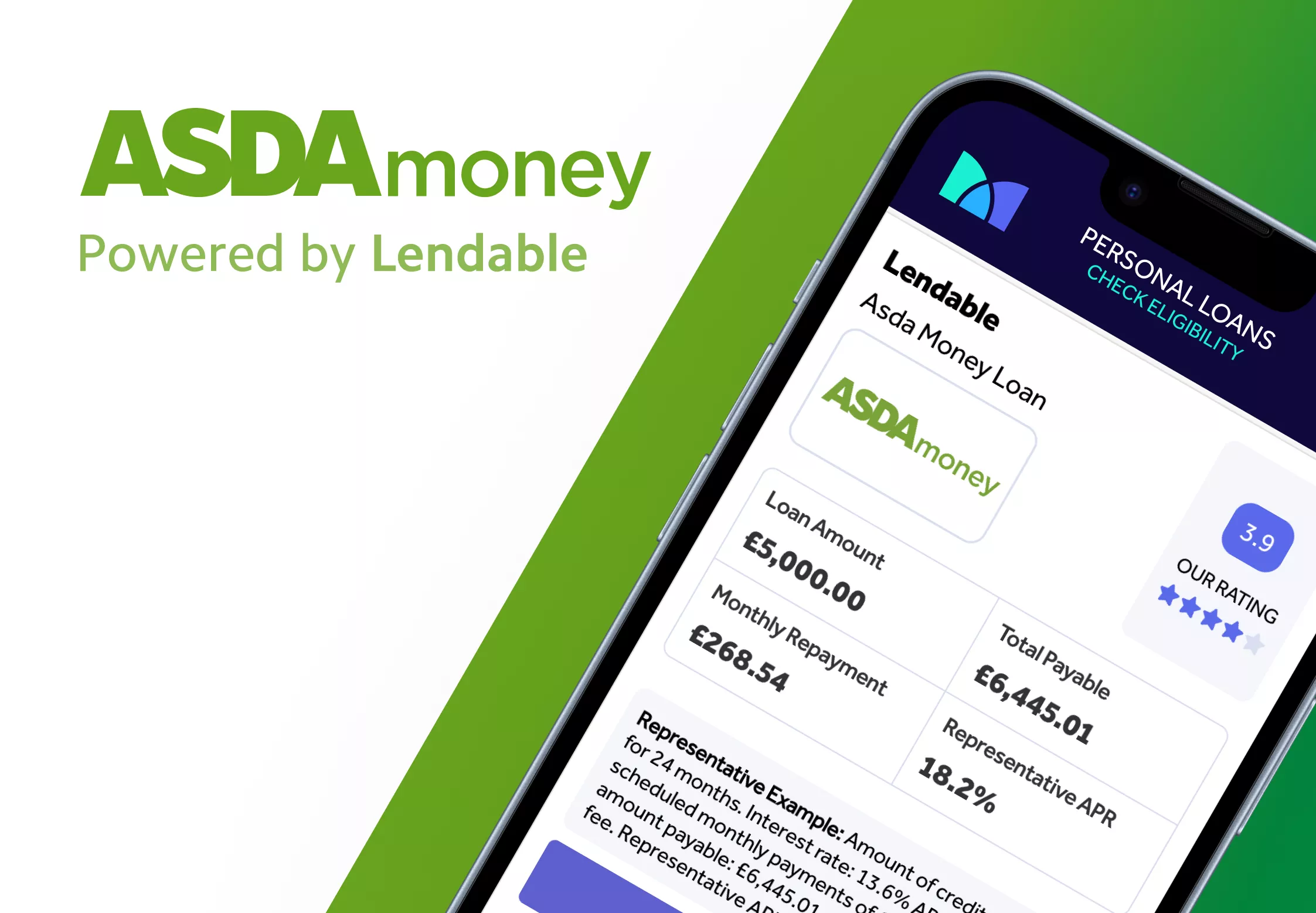

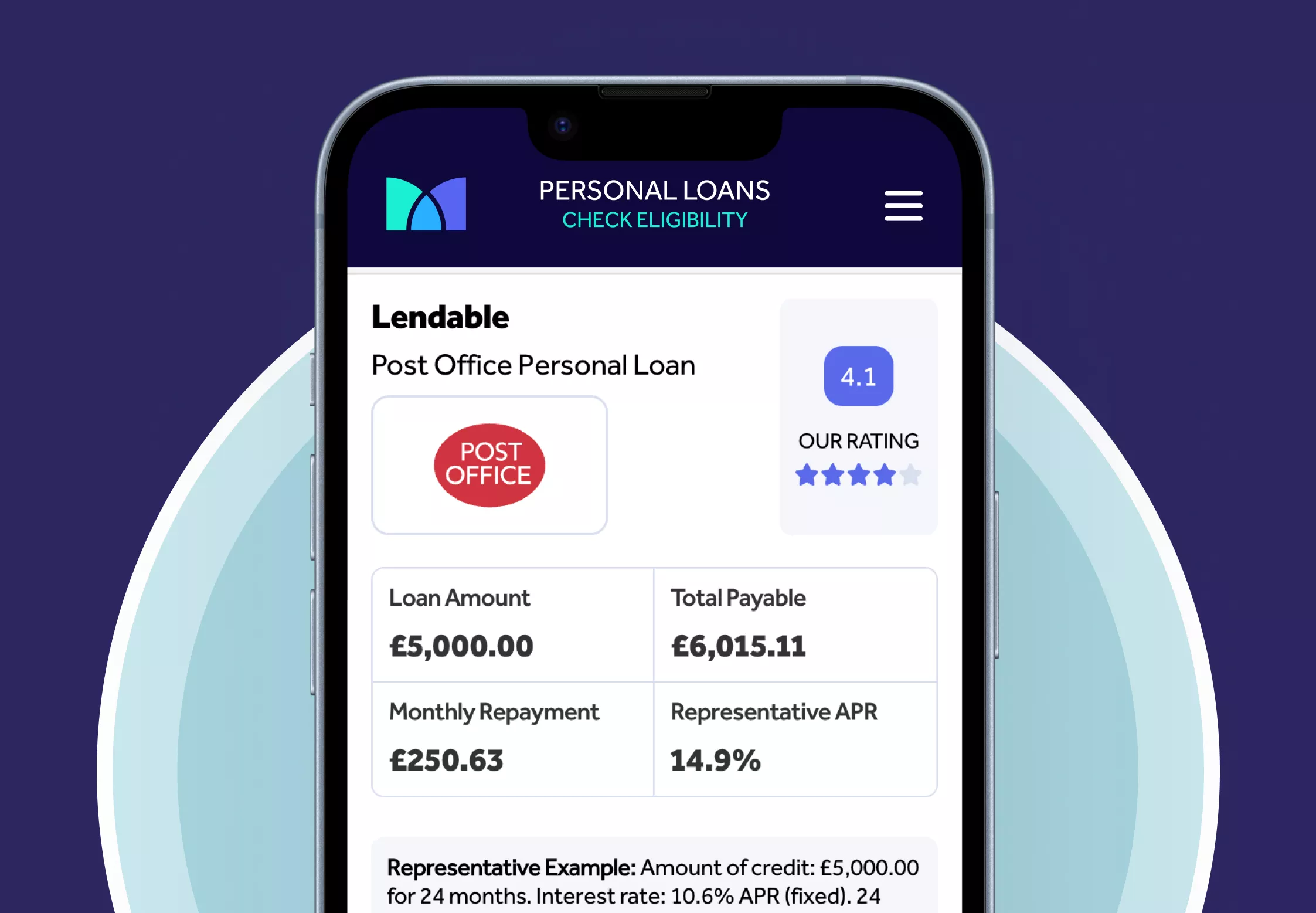

Lendable Loans Review

How to Apply for a Car Loan in the UK

My Community Finance

Asda Loans Review

Post Office Loans Review

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity. Mintify is an Introducer Appointed Representative of Creditec Limited. We provide editorial reviews of the whole market, but we only provide links to apply for products available through Creditec’s panel of lenders. We may earn a commission if you click these links. This does not affect our editorial independence, but it limits the products you can apply for directly on this site.