Credit Cards for everyday spending

Editor, Consumer Finance: Michelle Blackmore

Last Updated: February 7, 2026

In This Article

Do you really need a credit card for everyday spending?

For some people, it can make life easier by having one specific credit card covering the weekly shop, travel or bills, potentially earning rewards or helping to build a credit record over time when used responsibly.

For others, a debit card or a budgeting app might do the job just as well.

This guide walks you through how everyday credit cards work, what to look for, compare a few options and the alternatives worth considering.

What is an everyday credit card

An everyday credit card is designed for routine use, from groceries and fuel to daily coffees or metro costs. Unlike specialist cards such as balance transfer or 0% purchase cards, these provide ongoing flexibility rather than short-term promotional rates. That’s not to say a 0% purchase card couldn’t be used for day-to-day spending, but it’s usually better suited to spreading the cost of a larger purchase interest free for a set period.

Some of the typical features of an everyday card include:

- A consistent purchase APR instead of introductory rates

- Simple cashback or reward points

- Contactless, app-based and digital wallet support

If you are focused on rewards or cashback, remember that some everyday credit cards charge fees: from small monthly amounts to higher annual costs. Whether a card is worth it depends on your affordability and how you plan to use it. Always ensure the value of any rewards or cashback outweighs any fees and that you can afford to repay what you spend in full each month.

Who might an everyday credit card suit

Everyday credit cards can suit a wide range of people, depending on how they use credit and manage repayments. They can work well for those who want a straightforward card for daily spending, prefer predictable terms, or are looking to build credit over time. The key is to use the card responsibly and make regular repayments in full whenever possible.

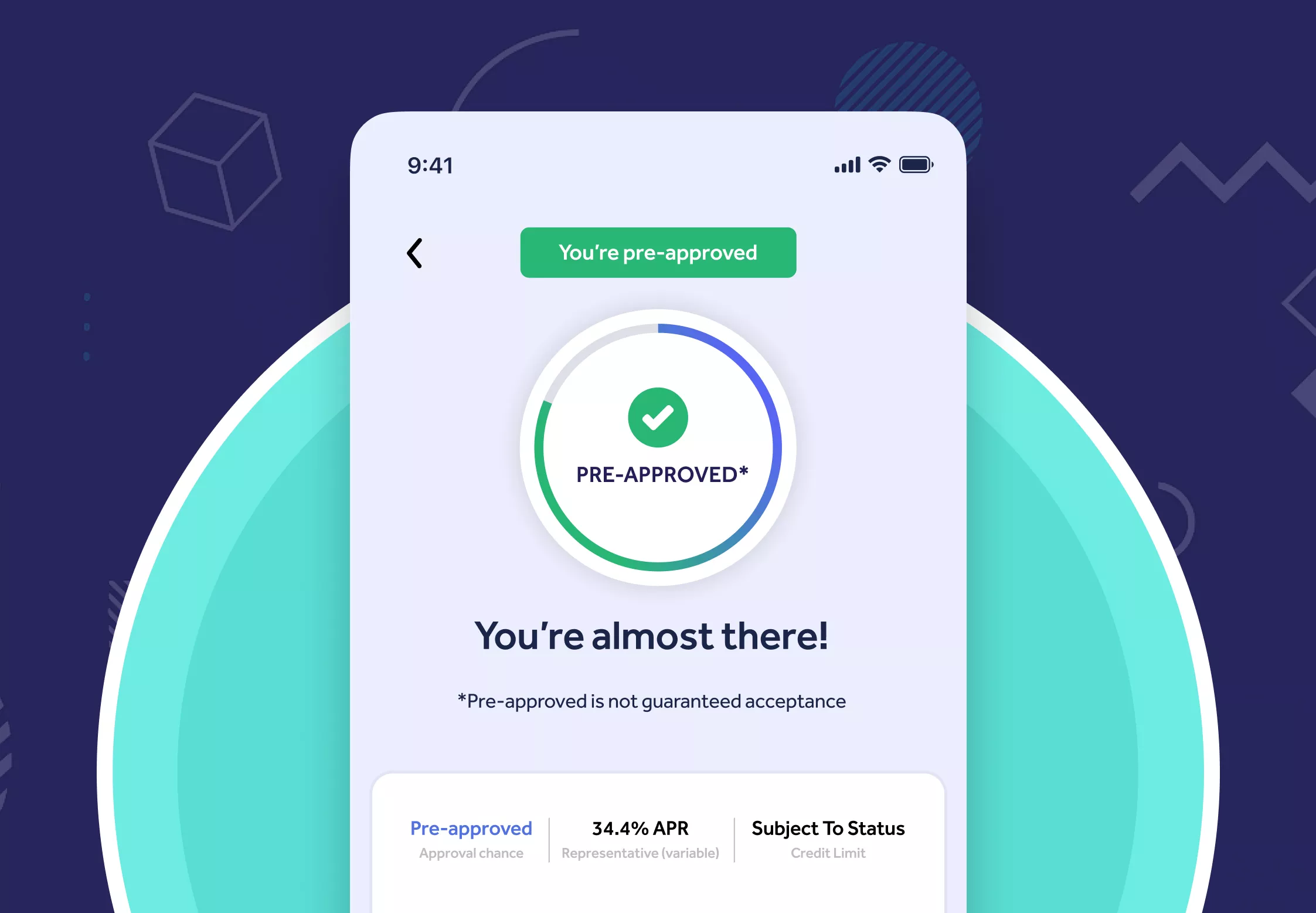

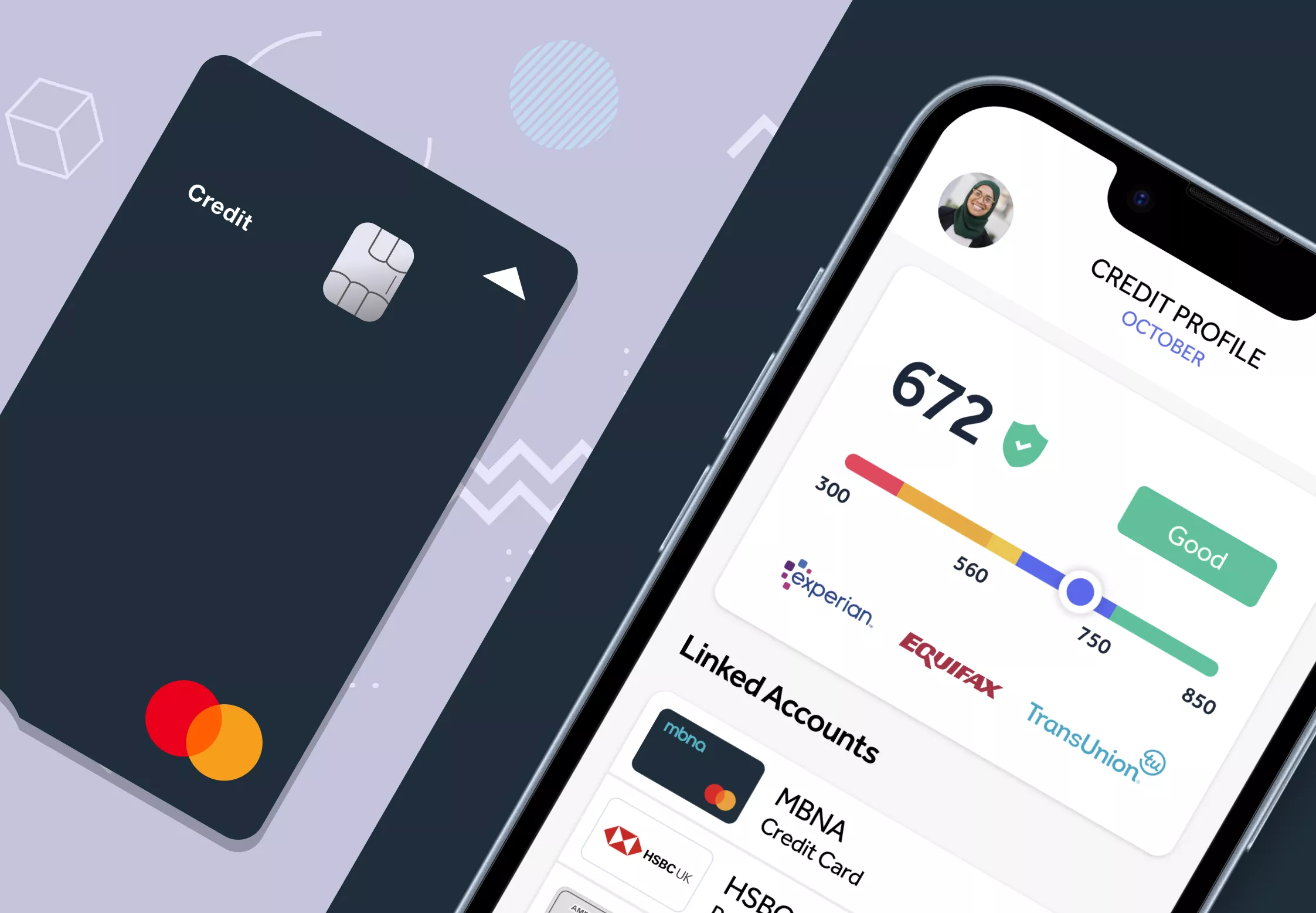

If you pay off your balance each month, an everyday card with rewards or cashback could offer steady value on your normal spending. If you sometimes carry a balance, you might prefer a card with a lower ongoing interest rate instead. Checking your credit card eligibility before applying helps you see your likelihood of approval without affecting your credit score and avoids unnecessary hard searches on your credit report.

Mintip: Take a moment to think about how you plan to use a credit card. If you already carry balances elsewhere, applying for another card could increase your total borrowing and interest costs.

Find the right Credit Card for you

No impact to your credit score

Find out which cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

How to choose the right everyday credit card

Choosing the right card comes down to how you use credit, how often you repay in full, and what you value most whether it’s flexibility, rewards or low interest. It’s worth comparing a few options before you apply so you can find one that matches your spending habits and what you can comfortably afford to repay.

Understand your spending pattern

Look at how you usually spend and repay. If you clear your balance in full each month, you can focus on cards that offer rewards or cashback. If you tend to carry a balance, it’s better to look for one with a lower ongoing purchase rate to help keep borrowing costs manageable.

Compare the APR offered to you

You will see a representative APR, which shows the typical cost of borrowing for at least 51% of successful applicants. The rate you are offered personally may be higher or lower depending on your credit profile and the lender’s assessment. If you do not clear your balance in full each month, even a small difference in APR can increase the total interest you pay over time. Always check the representative example and ensure you understand how interest is calculated before applying.

Check the interest-free period

Most credit cards offer up to 56 days interest free on new purchases, provided you pay the full balance each month. This can help manage short-term cash flow, but once you carry a balance forward, the interest-free period usually no longer applies. Missing a payment or only paying the minimum may also mean you lose this benefit.

Check for fees

Some cards charge annual fees. Always weigh these against any cashback or rewards to make sure you’re not paying more in fees than you earn in benefits. If the card has an annual or monthly fee, factor this into your total yearly cost.

Look for extra value

Some cards offer additional features such as no fees on foreign transactions. These benefits can make a difference if you regularly shop online in a different currency or use your card for travel. Make sure you check whether these features apply automatically or require activation.

Use soft-search eligibility tools

Using a credit card eligibility checker lets you see which cards you’re more likely to be accepted for before you apply. It’s a soft search, so checking your eligibility won’t affect your credit score. This helps you compare cards safely without leaving a mark on your credit file.

Supermarket credit cards

Supermarket credit cards are linked to major UK grocery chains and reward you for everyday spending. They work like standard credit cards but often offer points, cashback or discounts when used in-store, online or at partner retailers.

When comparing supermarket cards, look at how rewards convert into real savings and whether the value outweighs any fees or interest charges. Always check the APR and terms offered to you through a soft eligibility check before applying, as rates and rewards can change.

Many major retailers such as Tesco, Asda, M&S and John Lewis offer their own branded cards, each with different reward structures such as Clubcard points, Asda rewards and other vouchers or points. Rewards can be useful if you pay your balance in full each month, but if you carry a balance, the interest charged may outweigh any benefit.

Below are some of the supermarket credit cards you might come across from well-known UK retailers. There are other cards on the market that may not appear here but could suit you better, depending on how you spend and what you value most.

John Lewis Partnership credit card vs M&S Bank Rewards credit card

NewDay Limited John Lewis Partnership Credit Card |  M&S Bank Rewards | |

|---|---|---|

| Account Fee | £0 | £0 |

| Representative APR | 29.90% | 23.90% |

| Purchases Description | 29.95% (variable) p.a. | 0% for up to 9 months, then 23.90% (variable) p.a. |

| Purchases Interest Free | 56 days | 55 days |

| Balance Transfers | 29.95% (variable) p.a. (5% fee) | 0% for 90 days, then 23.90% (variable) p.a. (3.49% fee) |

| Incentive on Opening | Start off with double points for 60 days when you open a John Lewis credit card: 10 points (instead of 5) for every £4 spent at John Lewis and Waitrose. | Enjoy £5 back in M&S vouchers for every £100 you spend with M&S for your first six months. |

| Cashback/Rewards (if applicable) | After the first 60 days, earn 5 points for every £4 spent on eligible purchases at John Lewis and Waitrose and 1 point for every £10 spent elsewhere. | 1 rewards point per £1 spent in M&S and 1 rewards point for every £5 spent elsewhere. 200 rewards points = £2 in M&S vouchers. |

| Minimum Credit Limit | £250.00 | £500.00 |

| Intro Balance Transfers Fee | 0.00% | 3.49% |

| Balance Transfers Fee | 5.00% | 3.49% |

| Foreign Usage (EU) | 2.75% | 3% |

| Foreign Usage World | 2.75% | 3% |

If you’re looking for a credit card that may help build your credit file while earning rewards on everyday supermarket spending, a handful of options combine both features. These cards often carry higher APRs than standard reward cards and are best suited if you repay on time.

Asda Money Select credit card vs Tesco Bank Foundation credit card

Asda Money Select Credit Card |  Tesco Bank Foundation | |

|---|---|---|

| Account Fee | £0 | £0 |

| Representative APR | 44.80% | 29.90% |

| Purchases Description | 39.8% (variable) p.a. | 29.9% (variable) p.a. |

| Purchases Interest Free | 56 days | 56 days |

| Balance Transfers | 39.8% (variable) p.a. | 29.95% (variable) p.a. (3.99% fee) |

| Incentive on Opening | Get £20 in your Cashpot when you spend at least £50 in the first 60 days and set up a direct debit. Offer available for a limited time only. | When you earn points, you can exchange them for vouchers to save on groceries and fuel or you can get twice the value when using them with Tesco Reward Partners. |

| Cashback/Rewards (if applicable) | Get 0.75% back on your Asda spend and 0.2% back everywhere else. | 5 points per £4 spent (£4 minimum) in Tesco, 1 point for every £4 spent on Tesco fuel (excluding Esso) plus 1 point per £8 spent (£8 minimum) outside Tesco. 100 points = £1 in vouchers. Points are converted to Tesco vouchers or can be exchanged for Partner rewards to receive money off a variety of restaurants, entertainment or Avios points. |

| Minimum Credit Limit | £250.00 | £250.00 |

| Intro Balance Transfers Fee | 0.00% | 0.00% |

| Balance Transfers Fee | 0.00% | 3.99% |

| Foreign Usage (EU) | 2.99% | 2.75% |

| Foreign Usage World | 2.99% | 2.75% |

You can also read our guide on best credit cards to build credit for alternative options other than supermarket credit cards including credit building options that offer 0 introductory periods on balance transfers.

Carrying existing credit card balances

If you’re carrying balances on other credit cards, a balance transfer credit card can help you pay it down faster by moving your balance to a new card with 0% interest for a set period. Using a balance transfer calculator helps you understand how much interest you could potentially save by transferring debt from your existing cards to a balance transfer card.

Responsible use and credit impact

Used carefully, a credit card may help support or build your credit profile by showing that you can borrow and repay on time. Paying the balance in full each month, staying within your credit limit, and making payments on time all demonstrate good account management to lenders. Over time, this can have a positive impact on your credit record, though results vary by individual circumstances.

However, missing payments or carrying high balances can harm your credit score and lead to extra interest or late payment fees. Carrying a balance over several months can also lead to persistent debt. If possible, try to pay off your balance in full each month to stay within the interest-free period. Avoid withdrawing cash on your card, as this often incurs higher rates and charges.

Mintip: Credit cards can be useful tools for managing spending, but borrowing more than you can comfortably repay may lead to persistent debt. If you’re worried about keeping up with payments, speak to your lender early or get free support from StepChange Debt Charity or MoneyHelper

Credit card vs debit card for everyday spending

Both credit and debit cards can be used for daily purchases, but they work differently. A debit card spends your own money directly from your account, while a credit card lets you borrow up to a set credit limit from your credit card provider that must be repaid later.

Using a credit card can offer extra protection on purchases over £100 through Section 75 of the Consumer Credit Act, and may help build your credit record if you borrow and repay responsibly. However, it can also lead to interest or fees if you don’t repay in full.

Debit cards could help you stay within your budget and avoid borrowing costs.

For everyday spending, the best choice depends on your goals, repayment habits and how comfortable you are using credit. Credit is subject to status and individual approval.

Other alternatives worth considering

If you’re unsure whether a standard everyday credit card is the right fit, a few other types may suit your situation better. Each serves a different purpose, so it’s worth understanding how they work before applying.

- Credit builder cards: Designed for people with limited or recovering credit histories. They often have higher APRs but may help improve your credit profile if used responsibly and repaid on time.

- 0% purchase cards: Useful for spreading the cost of larger purchases without paying interest for a set introductory period. Always check when the 0% offer ends.

- Balance transfer cards: Allow you to move existing balances to a lower or 0% interest rate, helping to reduce interest costs and pay debt down faster. Be mindful of any transfer fees and ensure you make at least the minimum payment on time each month.

Each option has different eligibility criteria and costs. Think about what you need the card for and whether you’ll repay in full or carry a balance. Using credit card eligibility checkers can help you compare cards safely without affecting your credit score.

Choosing the right credit card starts with knowing your goals whether that’s building credit, spreading costs or reducing debt. Focus on affordability first and use eligibility checkers to compare options before committing to a credit card.

Key takeaways

- Everyday credit cards are best for ongoing, manageable spending rather than short promotional offers.

- Compare representative APRs, interest-free periods and fees before applying.

- Always consider affordability and repay in full where possible to avoid interest charges.

- Check your credit card eligibility first with a soft search so your credit score is not affected.

- If you already have existing balances, look at balance transfer cards to help reduce interest costs.

- Different cards suit different goals, from credit building to spreading costs or earning rewards; focus on what fits your situation.

Remember: All credit is subject to status, terms and individual approval. Always review the representative APR and total cost of borrowing before applying.

Find the right Credit Card for you

No impact to your credit score

Find out which cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

What is a balance transfer fee?

How to do a balance transfer on a credit card

Marbles credit card review – is it a good option to consider?

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.9% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Registered in England and Wales. Company Number: 15163923. VAT Registration Number: 498 4852 22.

Mintify® is a registered trademark of Mintify Limited in Great Britain and Northern Ireland under registration number UK00003974142. Data Protection ICO Registration Number: ZB601987.

Mintify® provides general information about the attributes and characteristics of financial products and their providers. Our services are intended for UK residents only and are offered on a non-advised basis for informational purposes. We do not charge users any fees for our services and do not recommend specific products or providers. We may receive commission, but only via our FCA-regulated introducer partner relationships (iARs), and never directly from the product providers themselves. Learn more about how we fund this site.

Mintify Limited, trading as Mintify®, is an Introducer Appointed Representative of Creditec Limited. Creditec Limited acts as a credit broker, not a lender, and is authorised and regulated by the Financial Conduct Authority (FRN:1023899). Mintify may introduce you to Creditec Limited to provide you with an information-only comparison service for credit products from a range of credit providers. Creditec will not charge you a fee for using their services. Creditec Limited is authorised and regulated by the Financial Conduct Authority and is entered on the Financial Services Register under reference number: 971164. Creditec Limited is registered in England and Wales under company number 13700425; registered office: The Steam Mill Business Centre, Steam Mill Street, Chester, United Kingdom, CH3 5AN. FRN. 971164. ICO registration number: ZB288703

While we strive to ensure the information on this site is up-to-date and accurate, we make no representations, warranties, or guarantees, whether express or implied, regarding the completeness, accuracy, or suitability of any information provided. All information is provided “as is” and should not be relied upon without verification. You should confirm any details directly with the relevant product or service provider and review all information they provide thoroughly. If you are uncertain, we strongly recommend seeking independent advice before applying for any product or entering into any agreement.

© 2023 – 2025 Mintify Limited. All Rights Reserved.

6501, 321-323 High Road, Chadwell Heath, Essex, RM6 6AX