Can foreigners get personal loans in the UK?

Editor, Consumer Finance: Michelle Blackmore

Last Updated: March 2, 2026

In This Article

Quick Answer: Yes, it’s possible, but most lenders will ask for a UK bank account, proof of address and income, and a valid visa that allows you to work or study. Each lender’s requirements can vary.

Moving to the UK, or any new country, often means starting your financial life from scratch and that includes building a credit profile in your new home. This can feel frustrating, especially if you already have a strong credit history elsewhere, but UK lenders must carry out their own due diligence before offering credit.

If you’re a foreign national, getting a Personal Loan is possible, but it isn’t always straightforward. Most lenders will want to see proof that you live and earn income in the UK and that repayments are affordable based on your circumstances.

This guide explains how personal loans work for foreign residents, what lenders look for, how visa status and credit history affect eligibility, and what you can do to improve your chances of approval over time.

Visa and residency play a role in getting a personal loan

Your visa and residency status influence how lenders assess your application. Most lenders need to confirm that you are legally living in the UK and that your right to remain covers the full length of the loan term. This helps them ensure repayments are affordable and sustainable during your stay.

- Work visas: Some lenders may view applications more positively where a stable income and a visa allowing employment are in place.

- Student visas: It can be more difficult to access mainstream personal loans while studying. Some students may qualify if they have part-time work, a guarantor or a credit history in the UK, but many choose to focus on building credit first.

- Family or partner visas: If you live in the UK as part of a household with joint income, you may meet eligibility requirements provided you can show regular income and affordability.

- Permanent residency or settled status: Those with indefinite or long-term residency rights are often assessed in the same way as UK citizens and may have a wider choice of lenders.

Lenders will also ask for proof of identity, address and immigration status during application. Keeping your documents current and consistent across your bank and credit accounts helps prevent delays and improves the accuracy of your credit record.

Building a UK credit history

If you have recently moved to the UK, lenders will usually not be able to see your overseas credit record. Each country has its own reporting system, and information is typically not transferred between them. This means you will need to build your credit history from the beginning.

A good first step is registering on the electoral roll if you are eligible, paying household bills in your name, and keeping your bank account and address information consistent. These actions help credit reference agencies record your payment history and confirm your identity.

Another useful starting point is applying for your first credit card in the UK. Using it for small purchases and paying it off in full each month shows lenders that you can manage credit responsibly. Over time, this can help you build a positive payment record and strengthen your UK credit profile. If you travel frequently or make purchases in other currencies, you may want to explore credit cards that charge no foreign transaction fees. Read our full guide on credit cards with no foreign fees for more details.

Even if your credit history is limited, maintaining steady income, low levels of borrowing and regular on-time payments across bills and accounts can improve your profile over time. Many lenders also offer tools to check your eligibility safely before applying, which helps you monitor progress without affecting your credit score.

Mintip: Some lenders, such as Yonder, use open banking to verify income and address instead of relying only on a credit score. This approach may make it easier for newcomers to start building a UK credit record.

Get Personalised Loan Rates

Find lenders that may be able to approve you

Options for all credit backgrounds

Representative 32.9% APR

No impact to your credit score

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Loan options available for foreign nationals

Once you have some UK credit history and a steady income, you may be able to apply for different types of loans. The options available will depend on your circumstances, visa length and affordability.

- Unsecured personal loans: Unsecured personal loans are offered by banks, building societies and regulated online lenders for general borrowing needs such as home improvements or consolidating debt. You will usually need a regular income and a record of managing credit in the UK.

- Guarantor loans: A UK-based guarantor can support your application by agreeing to make repayments if you cannot. This can help if your own credit record is still short or incomplete.

- Community or credit-union loans: Credit unions and local lenders may provide small, affordable loans for people who live or work in their area. They focus on affordability and can be a practical option for new residents building financial stability.

- Digital lenders: Some digital lenders use open banking data to assess affordability. This may make it easier for applicants with regular income but limited credit history to be considered.

Before applying, check each lender’s representative APR, eligibility rules and repayment terms carefully. Always make sure repayments fit within your budget and use a soft-search tool first if available.

How to check your eligibility as a foreigner in the UK

Before applying for a loan, it’s sensible to see which lenders are likely to accept you. This is especially important if you’re new to the UK and your credit record is still building. Making several full applications in a short time can lower your credit score, so it’s best to check eligibility first.

- Use a soft-search tool: These run a soft credit check that shows your likelihood of approval without affecting your score. This helps protect your record while you explore genuine options.

- Review representative APRs: The advertised rate is only an example. Your actual rate depends on your income, visa status and credit profile. Comparing lenders gives you a realistic view of potential costs.

- Check your details match: Ensure your name, address and employment details are consistent across your bank, credit and visa documentation, as mismatches can trigger automated declines.

- Read the terms carefully: Look at the total cost, repayment schedule and any early repayment fees before applying.

If you’re new to the UK and have limited credit history, you may not see many results when using a soft-search tool at first. This is normal and will improve as you build a track record of paying bills and managing accounts in your name. If you don’t see suitable options, you can contact lenders directly to explain your situation and ask what information they consider for new residents. Always confirm whether they run a hard or soft credit check before you proceed, as hard checks can temporarily lower your score.

Using an eligibility checker can still be helpful. It highlights lenders that use alternative data, such as open banking, so you can compare options safely before applying.

What to do if you’re not eligible yet

If you’re new to the UK and find that lenders can’t offer you a loan yet, it usually means they don’t have enough local information to assess your application. That’s normal at the beginning. The UK credit system relies heavily on national data, so even if you had an excellent record in your home country, lenders here cannot access it. The goal now is to build that history step by step.

- Open and use a UK bank account: Make sure your salary, rent and everyday payments go through the same account. Lenders and credit agencies use this to verify your income and stability.

- Register your address properly: Whether renting or staying temporarily, keep your address consistent across your bank, mobile provider and bills. Frequent changes can delay credit file creation.

- Put bills in your name: Having a mobile phone contract or household utility account in your own name helps credit reference agencies link regular payments to you, gradually building your UK credit record.

- Use small forms of credit: Start with a credit builder card or retail finance agreement and pay it off in full each month. This shows lenders that you can manage credit responsibly under UK rules.

- Show income continuity: Provide payslips, employment contracts or invoices if you are self-employed. Regular deposits into your account make affordability easier to demonstrate later.

- Be patient with timeframes: It can take six to twelve months of activity before your credit history becomes strong enough for mainstream lenders to assess confidently.

- Ask lenders about alternative data: Some digital lenders now use open banking or rent-payment data to assess applications. These options may appear sooner than traditional credit scores.

It’s understandable to feel frustrated if you have strong finances elsewhere but are still seen as “new” in the UK. The key is to focus on visibility and consistency keeping income, payments and addresses aligned so your UK profile builds quickly and accurately.

Mintip:If you want to track your credit progress in the UK, Mintify is building an intelligent budgeting app and financial control centre for your money. It helps you budget, track spending, set achievable goals, and plan your financial future, all in one place. Get early access and we’ll let you know as soon as it launches.

Building credit confidence in the UK

Getting started with credit in a new country takes time, but every step you take helps lenders see a clearer picture of your finances. Managing your money through one bank account, paying bills on time and staying consistent with your details will gradually strengthen your UK credit profile. Over time, this makes it easier to access loans and other financial products on fairer terms.

Frequently asked questions

Can I get a loan in the UK without a UK credit history?

It’s possible, but more difficult. Lenders rely on UK credit data to assess risk, so if you’re new to the country they may not have enough information yet. You can improve your chances by building your credit record through a bank account, bills in your name, or a credit card used responsibly. Some newer lenders also use open banking data to assess affordability instead of traditional credit scores.

Can I use my overseas credit history in the UK?

No. Credit records are not transferable between countries. UK lenders only see information held by UK credit reference agencies such as Experian, Equifax or TransUnion. However, having a strong financial background elsewhere can still help when you discuss your application directly with a lender or employer, even if it doesn’t appear on your UK credit file.

Do I need a visa to get a loan in the UK?

Yes, if you’re not a UK citizen, lenders will ask for proof that you have the legal right to live and work in the UK. Your visa should normally last for at least as long as the loan term. Short-term or expiring visas can limit what lenders are willing to offer.

Can international students get personal loans?

Most mainstream lenders don’t offer personal loans to students, but there are other ways to borrow responsibly. Some banks provide student overdrafts or credit cards with small limits, and certain digital lenders may consider applicants with income from part-time work. Always check the repayment terms and consider whether borrowing is necessary while studying.

How long does it take to build credit in the UK?

It usually takes six to twelve months of consistent activity to create a visible UK credit profile. Paying bills on time, using a credit card carefully, and keeping your details up to date across accounts all help. Over time, this makes it easier to qualify for mainstream loans on better terms.

What documents will I need to apply for a loan?

Lenders typically ask for proof of identity, UK address, income and immigration status. This can include your passport or biometric residence permit, recent payslips or tax returns, and a utility bill or tenancy agreement in your name. Having these ready helps avoid delays during assessment.

Key takeaways

- You can get a personal loan in the UK as a foreign national, but lenders will check your visa, income and UK residency details.

- Your overseas credit record is not visible to UK lenders, so start building a UK credit history early.

- Keep your address, income and identification details consistent across accounts to avoid delays.

- Open banking lenders and small starter loans may offer early options while your UK profile develops.

- Time, stability and regular on-time payments are key factors that improve your chances of eligibility.

Get Personalised Loan Rates

Find lenders that may be able to approve you

Options for all credit backgrounds

Representative 32.9% APR

No impact to your credit score

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Related Articles

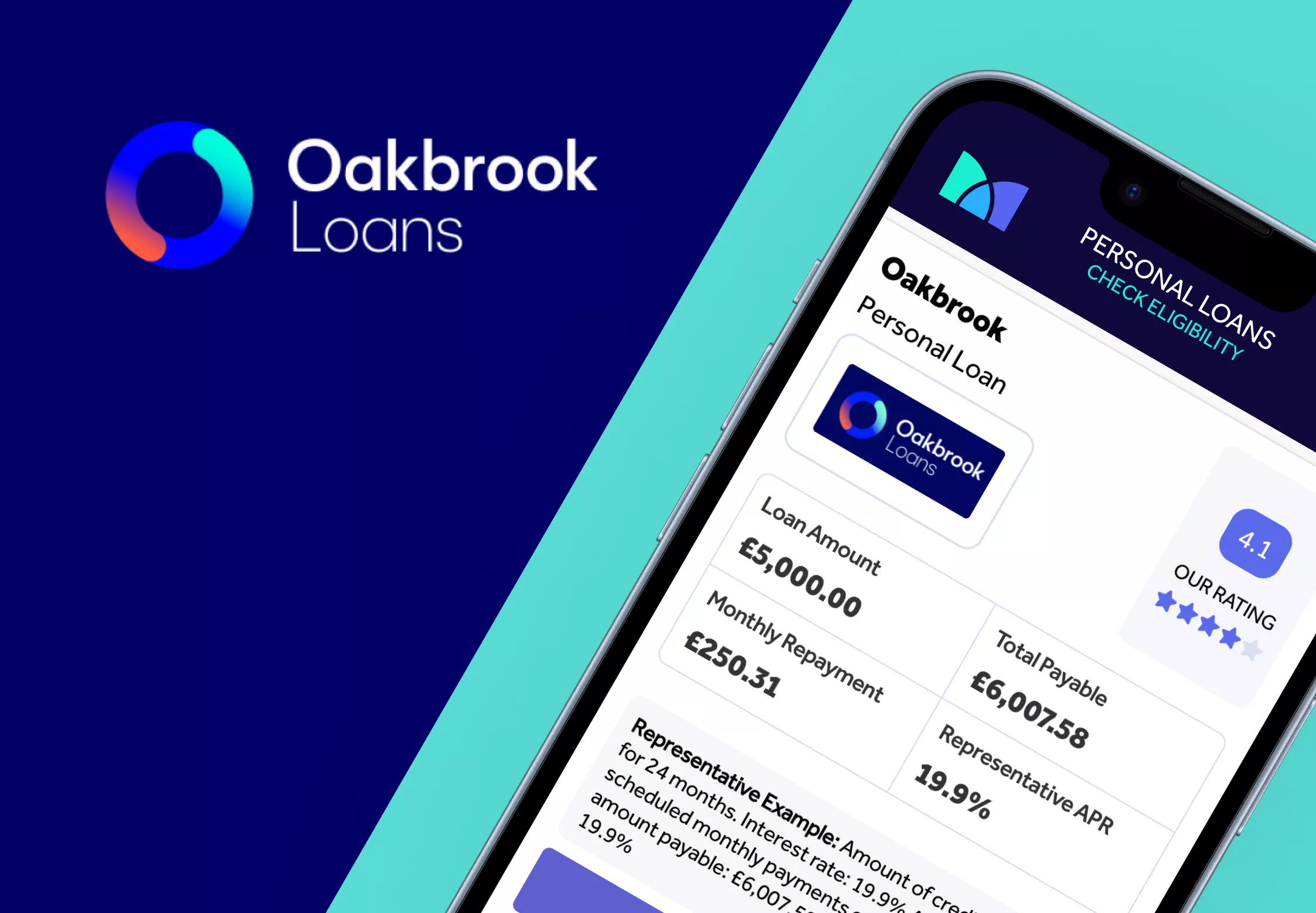

Oakbrook Loans Review

Lendable Loans Review

How to Apply for a Car Loan in the UK

My Community Finance

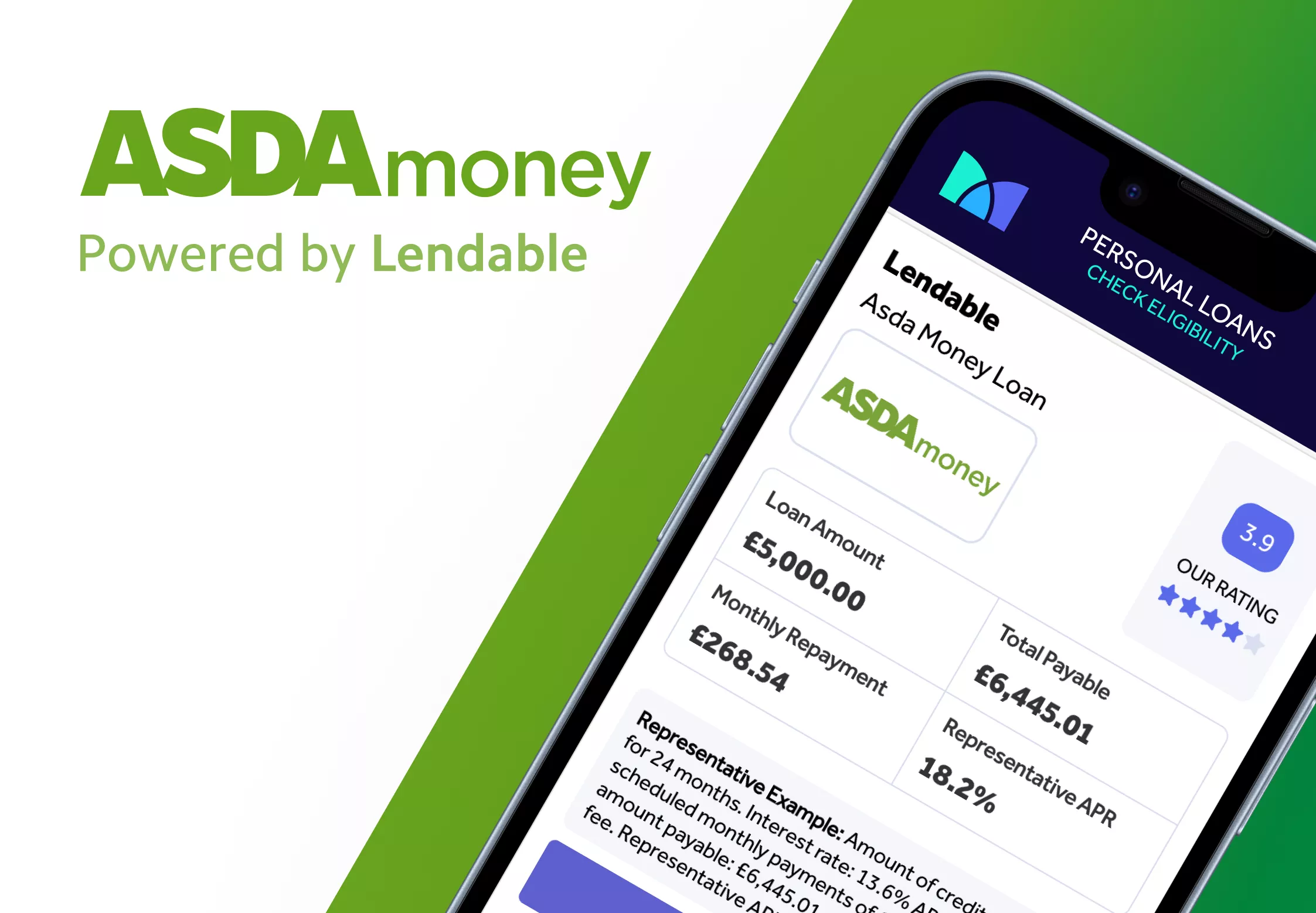

Asda Loans Review

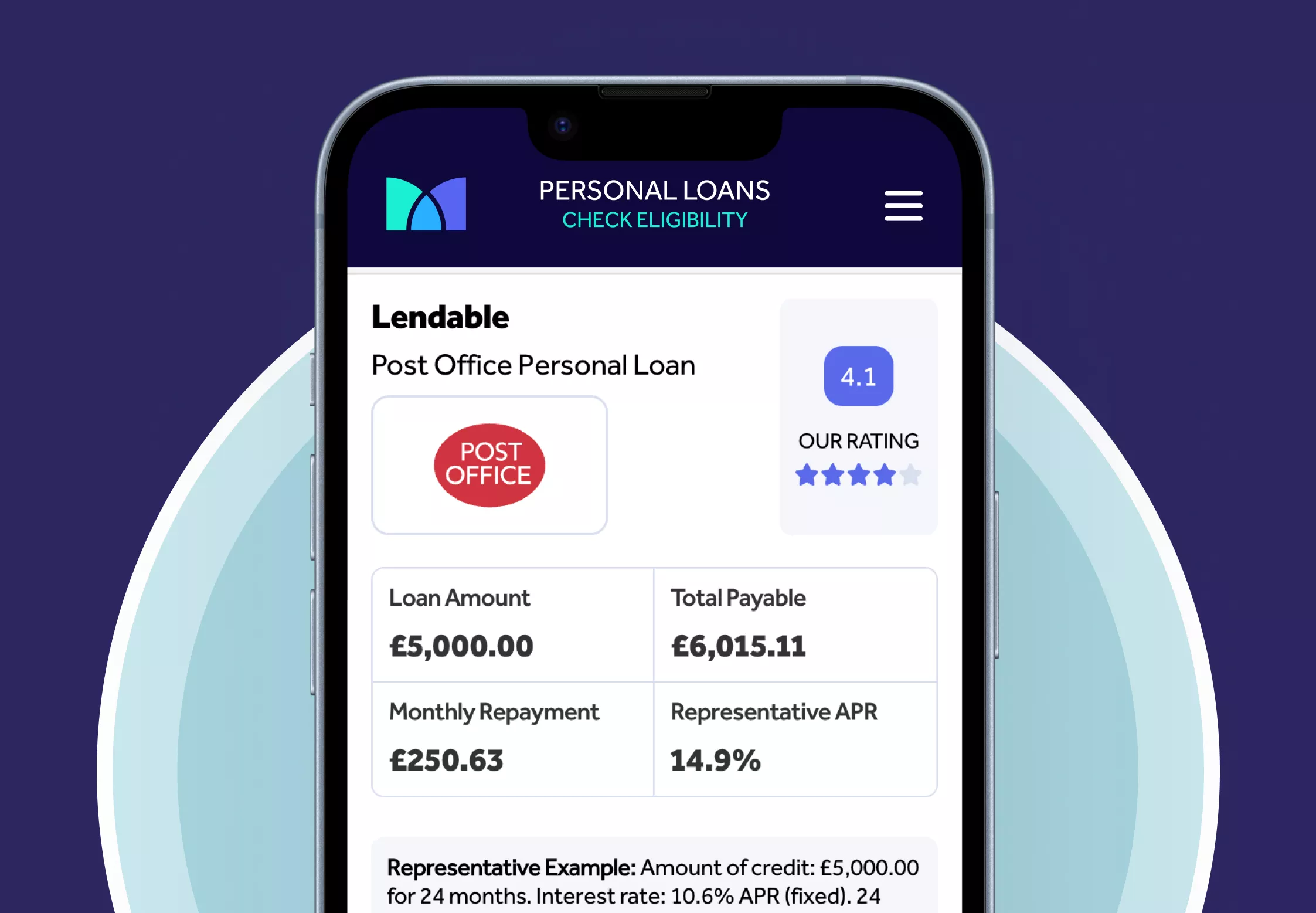

Post Office Loans Review

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity