Aqua Credit Card Review and Eligibility Requirements

Editor, Consumer Finance: Michelle Blackmore

Last Updated: January 17, 2026

In This Article

Aqua credit cards, issued by NewDay Ltd, are a well-known option in the UK for those who want to build or improve their credit profile. While often linked with credit card offers for bad credit or credit cards for a low credit score, they are not exclusively for this group. Aqua cards can also be a stepping stone for consumers looking to strengthen their credit record through responsible borrowing. or even consumers who are looking to get their first credit card.

This guide explores the types of Aqua credit cards available, who owns Aqua, how eligibility works, and what independent reviews say about the brand.

What type of credit cards does Aqua have?

Aqua offers two main credit card products:

- Aqua Classic: Designed to help customers build or rebuild their credit score, with manageable credit limits and access to financial tools.

- Aqua Balance Transfer: A short 0% balance transfer option (usually up to five months) that may be accessible to those who do not qualify for longer balance transfer deals elsewhere.

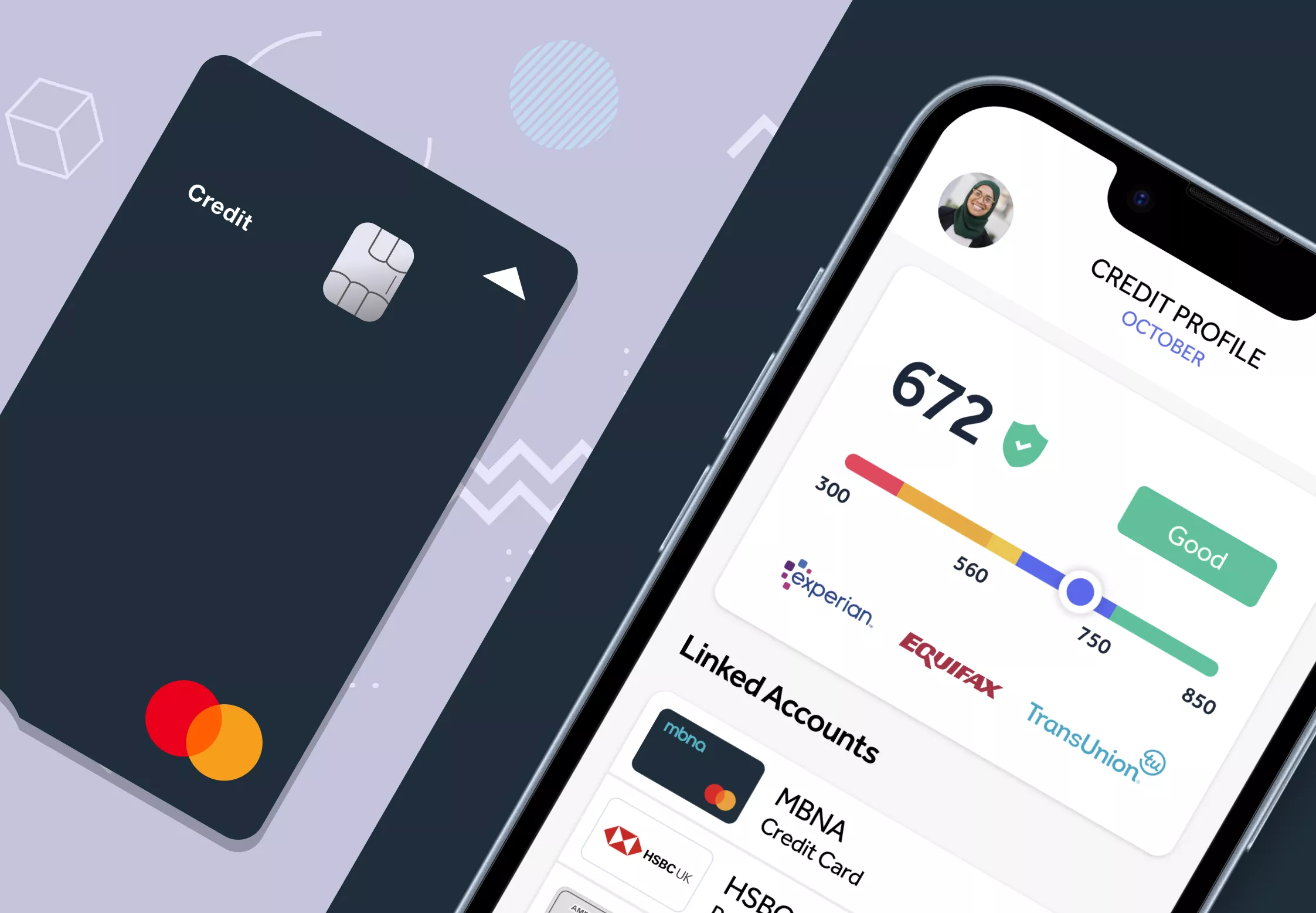

Both cards report account activity to the main UK credit reference agencies. Used responsibly, they can help to build or improve a credit score over time.

Who owns Aqua?

Aqua is owned and issued by NewDay Ltd, a UK-based financial services company. Some key information about NewDay is:

- NewDay specialises in consumer credit and manages several brands including Aqua, Marbles, Fluid, and Bip.

- NewDay Ltd is also the lender behind the John Lewis Partnership credit card.

- The company focuses on offering credit to a wide range of UK customers, including those who may find it difficult to access mainstream lending.

- Aqua has grown into one of NewDay’s main brands recognised for credit building solutions.

Explore and compare more NewDay credit cards on our dedicated page.

Why should I apply for an Aqua card?

Applying for any credit card should involve comparing options and checking your eligibility first. Aqua may be considered by people with lower or limited credit histories, but features may also appeal more broadly:

- Personalised credit limits: Aqua sets credit limits based on your profile, with the possibility of increases over time if the account is well managed.

- Fraud protection: 24/7 monitoring and security tools aim to keep your card safe.

- Aqua Coach: A feature in the Aqua app that allows you to track your credit score, see what affects it, and learn how to improve it.

- Digital payments: You can add the card to your mobile wallet for fast and secure in-store or online purchases.

- Potential upgrades: In some cases, customers with strong credit profiles and consistent account management may be invited to upgrade to Aqua Gold, which offers enhanced features.

- Exclusive offers: Aqua provides access to discounts, prize draws and partner deals, ranging from events and holidays to shopping rewards.

These features are intended to reward responsible credit use, but whether Aqua is right for you will depend on comparing it with alternatives in the market.

Mintip: If you miss payments, exceed your limit, or fail to manage your account responsibly, this will negatively affect your credit rating and may make borrowing more expensive or difficult in the future.

What are the eligibility requirements for an Aqua credit card?

To apply for an Aqua credit card, you will usually need to meet the following requirements:

- Age: You must be at least 18 years old.

- Residency: You should be a UK resident with a permanent UK address.

- Bank account: You must have a current UK bank or building society account.

- Source of income: Applications are accepted from people with income from employment (full-time or part-time), self-employment, or student income. Those without any income or who are unemployed are unlikely to be eligible.

- Credit history: You should not have been declared bankrupt within the past 18 months, nor have ongoing bankruptcy proceedings. Applicants who have received a County Court Judgement (CCJ) in the last 12 months will also typically not qualify.

- Existing accounts: You cannot usually apply if you have held an Aqua card in the past 12 months

- Contact details: A valid UK mobile phone number is required.

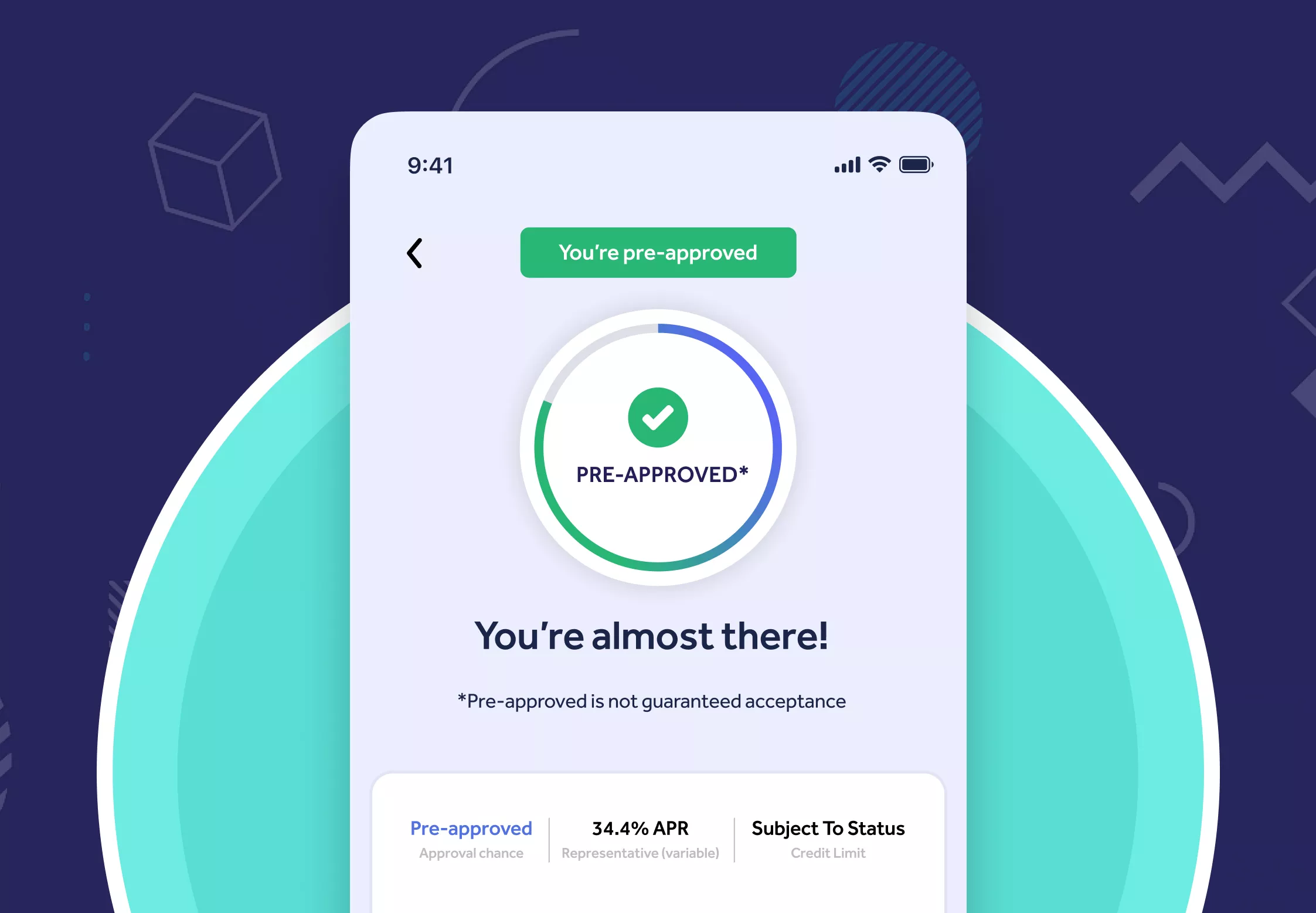

Aqua cards are often considered by people looking to build or rebuild credit, but they are also open to those applying for their first credit card. Meeting these requirements does not guarantee approval, as a credit and affordability check will still be carried out.

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.4% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Aqua balance transfer card features

Aqua’s balance transfer card is designed for customers who want to move existing debt while also building credit.

- 0% interest on balance transfers, typically for a short introductory period (often up to five months).

- Balance transfer fee applies (around 3%, minimum £3).

- Transfers must usually be made within 60 days of opening to qualify for the full promotional rate.

- You can transfer up to 90% of your available credit limit.

- If you miss payments or go over your limit, the promotional 0% period is withdrawn.

This card may be useful for those with a weaker credit file who cannot access longer 0% deals, though mainstream banks often offer much longer introductory balance transfer periods.

Are there better credit cards for balance transfers?

Whether there are better balance transfer cards than Aqua depends on your personal circumstances, including your credit history, the amount you want to transfer, and how long you need the 0% introductory period to pay it off without interest.

Here is how Aqua compares with some alternatives. Offers and eligibility can change, so always rely on the terms presented by the lender in your own offer.

| Card | Key Features | Who this may suit |

|---|---|---|

| Aqua Balance Transfer | Shorter 0 introductory period. | Smaller balances to transfer and access to limited options. |

| HSBC balance transfer | Longer 0% period; Ideal for larger balances. | Stronger credit scores and larger balances. |

| Vanquis balance transfer | Variety of different 0% offers based on credit profile. | Wide variety of credit profiles due to the various 0% offers. |

| Capital One Balance Transfer | 0% interest for up to 18 months, based on profile. | Available even if you’ve had CCJs or defaults in the past. |

The key point is that eligibility varies. If you have a stronger credit file, you may qualify for longer 0% introductory offers with mainstream banks. If your credit history is weaker, shorter-term options like Aqua or Vanquis may be more realistic.

This is why it’s important to use a free credit card eligibility check before applying. A soft search allows you to see which balance transfer cards you could be pre-approved for without affecting your credit score. This not only protects your credit record but also ensures you are comparing realistic options that match your profile.

Mintip: Ensure you can repay your balance transfer before the 0% ends or the standard APR will apply and increase your total cost; late or missed payments can end the offer early so check your contract for such clauses.

Customer Reviews: What do customers say about Aqua?

Customer feedback on independent review sites such as Trustpilot, presents a mostly positive picture. Many reviewers highlight an easy-to-use website and app, a quick application process, clear communication, and usefulness for building credit, while others report issues with payment processing (e.g. direct debits or phone payments) and occasional customer service delays. The points below group common positives and criticisms to help you compare cards.

Positive comments include:

- Credit limit increases proactively given.

- Excellent customer service and communication.

- Easy to use and ability to rebuild credit scores.

Critical feedback often mentions:

- Shorter balance transfer periods compared to other options.

- Some experience issues with direct debit options.

- Starting credit limits are lower.

Trustpilot reviews reflect individual customer experiences and are subjective to their own personal experience.

Overall, Aqua is often described as beneficial for those who use it responsibly to build credit, but less appealing to borrowers who are eligible for longer introductory offers, premium rewards or lower ongoing interest rates.

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.4% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.

Conclusion: Are Aqua credit cards worth it?

Aqua credit cards can be a practical option for those in the UK who want to build or improve their credit history. They are frequently associated with credit card offers for bad credit but should be seen more broadly as credit-building tools.

Key considerations

- Use an eligibility checker before applying.

- Manage spending within your limit and repay in full to avoid interest.

- Compare providers: longer balance transfer or lower APR cards may be available if your credit file allows.

With responsible use, Aqua can help improve your credit score and provide access to useful digital tools and features. However, the value of the card will depend on your circumstances and how it compares to other products available to you.

Frequently asked questions about Aqua

Is Aqua a credit card for bad credit?

Aqua is often used by people with lower credit scores, but it is better described as a credit building card. It can help improve your score through responsible use.

What is the maximum credit limit I can get with an aqua credit card?

The maximum credit limit depends on your individual credit profile. Aqua typically starts with lower limits to encourage responsible usage and may increase these over time as you demonstrate good financial habits.

Who owns Aqua credit cards?

Aqua is issued by NewDay Ltd, a UK-based financial services company that also manages brands such as Marbles, Fluid and Bip.

Does Aqua offer balance transfer deals?

Yes, Aqua offers a balance transfer card with a short 0% introductory period. Longer deals are available from other providers, depending on eligibility.

What is a credit card eligibility checker?

A credit card eligibility check is a soft search tool that assess your chances of approval for a specific credit card(s) before you apply, without leaving a mark on your credit file.

Can I use an eligibility checker for Aqua?

Yes. Using an eligibility checker lets you see if you could be approved for Aqua or other cards without affecting your credit score.

What’s the difference between eligibility and pre-approval?

Eligibility shows your likelihood of being accepted. Pre-approval means a lender has indicated you meet its criteria, subject to final checks. Pre-approval is not a guarantee, and the lender will confirm your information and run a full credit check before making a final decision.

Does Aqua have an app?

Yes. The Aqua app allows you to manage your account, track payments, and use tools such as Aqua Coach to monitor your credit score.

Related Articles

Check your credit card eligibility in the UK

Balance transfer cards for credit builders

How much can you balance transfer?

What is a balance transfer fee?

How to do a balance transfer on a credit card

Marbles credit card review – is it a good option to consider?

The content presented here has been impartially gathered by the Mintify team and is offered on a non-advised basis for informational purposes only. We adhere to strict editorial integrity

Find the right Credit Card for you

Does not impact your credit score

Find out which credit cards you’re eligible for

34.4% Representative APR (variable)

Mintify Limited, trading as Mintify, is an Introducer Appointed Representative of Creditec Limited who acts as a credit broker, not a lender.